Chicago Board of Trade (CBOT)

... "@" indicates the most recently auctioned US Treasury security eligible for delivery. Information contained in this publication is taken from sources believed to be reliable, but it is not guaranteed by the Chicago Board of Trade as to its accuracy or completeness, nor as to any trading result, and ...

... "@" indicates the most recently auctioned US Treasury security eligible for delivery. Information contained in this publication is taken from sources believed to be reliable, but it is not guaranteed by the Chicago Board of Trade as to its accuracy or completeness, nor as to any trading result, and ...

7. What Numbers Should Donors Use? and

... This study examines the impact of administrative inefficiency and donation price on donations to US NPOs using a better-specified model and industry-specific samples. …[Prior research studies do not test] donation price and administrative inefficiency in one model and only two test industry-specific ...

... This study examines the impact of administrative inefficiency and donation price on donations to US NPOs using a better-specified model and industry-specific samples. …[Prior research studies do not test] donation price and administrative inefficiency in one model and only two test industry-specific ...

annual report 2016 - Asseco Central Europe

... Selected items of Profit and loss account and Statement of cash flows for the period from 1 January 2016 to 31 December 2016 were recalculated at average exchange rate calculated from exchange rates announced by National Bank of Poland on the last day of each month in the reported period (EUR 1 = PL ...

... Selected items of Profit and loss account and Statement of cash flows for the period from 1 January 2016 to 31 December 2016 were recalculated at average exchange rate calculated from exchange rates announced by National Bank of Poland on the last day of each month in the reported period (EUR 1 = PL ...

Measuring Swedish Investor Sentiment Stock Market Response to

... The notion of how irrational beliefs held by investors affected the market by way of i.e. asset pricing and expected returns was presented by DeLong et. al. in 1990. In the model developed by DeLong et. al., some investors, denominated noise traders, were subject to sentiment – a belief about future ...

... The notion of how irrational beliefs held by investors affected the market by way of i.e. asset pricing and expected returns was presented by DeLong et. al. in 1990. In the model developed by DeLong et. al., some investors, denominated noise traders, were subject to sentiment – a belief about future ...

forms of business organization

... the sources and uses of cash during a period of time. The statement of cash flows shows the sources and uses of cash during a period of time. ...

... the sources and uses of cash during a period of time. The statement of cash flows shows the sources and uses of cash during a period of time. ...

![Accounting Consolidated Balance Sheets [ADVANCED HIGHER]](http://s1.studyres.com/store/data/000051389_1-9f43aeab3667ec7d058220f244bff4af-300x300.png)

Accounting Consolidated Balance Sheets [ADVANCED HIGHER]

... The ‘top part’ of the balance sheet treats all of the assets and liabilities of the subsidiary as if they were fully owned by the parent. No attempt is made to split items such as machinery or stocks into the amount owned by the parent, and the amount owned by the other shareholders. Instead, all of ...

... The ‘top part’ of the balance sheet treats all of the assets and liabilities of the subsidiary as if they were fully owned by the parent. No attempt is made to split items such as machinery or stocks into the amount owned by the parent, and the amount owned by the other shareholders. Instead, all of ...

Assessing profitability in competition policy analysis

... for which reliable data on cash flows and asset values is available over a sufficiently long time period. The methodology may be less suited for assessing future performance based on forecast data, or in cases where cost and revenue allocation or asset valuation are particularly complicated. ...

... for which reliable data on cash flows and asset values is available over a sufficiently long time period. The methodology may be less suited for assessing future performance based on forecast data, or in cases where cost and revenue allocation or asset valuation are particularly complicated. ...

RYDER SYSTEM INC (Form: 10-K, Received: 02/12

... additional maintenance services that are not included in their contracts. For example, additional maintenance services may arise when a customer’s driver damages the vehicle and these services are performed or managed by Ryder. Some customers also periodically require maintenance work on vehicles th ...

... additional maintenance services that are not included in their contracts. For example, additional maintenance services may arise when a customer’s driver damages the vehicle and these services are performed or managed by Ryder. Some customers also periodically require maintenance work on vehicles th ...

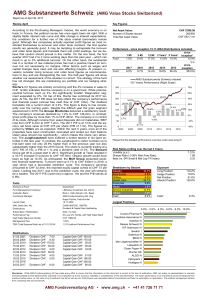

AMG Substanzwerte Schweiz (AMG Value Stocks

... slightly flatter interest rate curve and little change in interest expectations, the conditions for a further rise of the stock market barometers remain good. Although few companies actually reported profit figures as most restricted themselves to turnover and order book numbers, the first quarter r ...

... slightly flatter interest rate curve and little change in interest expectations, the conditions for a further rise of the stock market barometers remain good. Although few companies actually reported profit figures as most restricted themselves to turnover and order book numbers, the first quarter r ...

FORM 10-Q - 10K Wizard

... The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information, except to the extent such damages or losses cannot be limited or excluded ...

... The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information, except to the extent such damages or losses cannot be limited or excluded ...

Best Practices for Stable NAV LGIPs

... credits that have been approved by an independent credit analyst or internal credit committee, and the amounts must be deemed appropriate given the size and characteristics of the respective LGIP. The list of approved issuers should be documented in regular credit evaluations or formal credit meetin ...

... credits that have been approved by an independent credit analyst or internal credit committee, and the amounts must be deemed appropriate given the size and characteristics of the respective LGIP. The list of approved issuers should be documented in regular credit evaluations or formal credit meetin ...

Xero offers an attractive combination of growing

... Xero is a New Zealand-based software company that specialises in cloud-based SME accounting software delivered via an SaaS model. Since incorporation in 2006 the company has attracted 717,000 subscribers (as at March), implying market shares of around 55% in New Zealand, 21% in Australia, 4% in the ...

... Xero is a New Zealand-based software company that specialises in cloud-based SME accounting software delivered via an SaaS model. Since incorporation in 2006 the company has attracted 717,000 subscribers (as at March), implying market shares of around 55% in New Zealand, 21% in Australia, 4% in the ...

Chapter 6.1

... reports assets, liabilities, and owner’s equity on a specific date Income Statement: a financial statement showing the revenue and expenses for a fiscal period Net Income: the difference between total revenue and total expenses when total revenue is greater Net Loss: the difference between total rev ...

... reports assets, liabilities, and owner’s equity on a specific date Income Statement: a financial statement showing the revenue and expenses for a fiscal period Net Income: the difference between total revenue and total expenses when total revenue is greater Net Loss: the difference between total rev ...

Property Portfolio - Falcon Real Estate Investment

... properties that we have purchased and for which we have provided asset management, Falcon has earned a reputation for providing world class advisory services in U.S. real estate. For more information on our firm and updates on all of the other activities in which the company is engaged, please visit ...

... properties that we have purchased and for which we have provided asset management, Falcon has earned a reputation for providing world class advisory services in U.S. real estate. For more information on our firm and updates on all of the other activities in which the company is engaged, please visit ...

VEECO INSTRUMENTS INC (Form: 10-K, Received

... Advanced Packaging includes a portfolio of wafer-level assembly technologies that enable the miniaturization and performance improvement of electronic products, such as smartphones, smartwatches, and other mobile applications. As process steps such as wet etch and cleans in Advanced Packaging have b ...

... Advanced Packaging includes a portfolio of wafer-level assembly technologies that enable the miniaturization and performance improvement of electronic products, such as smartphones, smartwatches, and other mobile applications. As process steps such as wet etch and cleans in Advanced Packaging have b ...