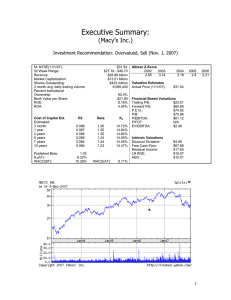

Macy's Inc. - Mark E. Moore

... and other consumer goods” (Dillard’s 10-K). As stated above, these 10-K reports show that creating a loyal customer base is crucial for success in this industry. With all of these firms selling the exact same types of merchandise, differentiation is extremely important in this market. ...

... and other consumer goods” (Dillard’s 10-K). As stated above, these 10-K reports show that creating a loyal customer base is crucial for success in this industry. With all of these firms selling the exact same types of merchandise, differentiation is extremely important in this market. ...

SMITH GROUP LARGE CAP CORE GROWTH FUND Institutional

... is generally higher than the rate expected for non-growth companies. If a growth company does not meet these expectations, the price of its stock may decline significantly, even if it has increased earnings. Growth companies also typically do not pay dividends. Companies that pay dividends may exper ...

... is generally higher than the rate expected for non-growth companies. If a growth company does not meet these expectations, the price of its stock may decline significantly, even if it has increased earnings. Growth companies also typically do not pay dividends. Companies that pay dividends may exper ...

Word - corporate

... Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) ...

... Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) ...

ABN AMRO Holding N.V.

... Unless otherwise indicated, the financial information contained in this Annual Report has been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union and IFRS as issued by the International Accounting Standards Board (IASB) which vary in certa ...

... Unless otherwise indicated, the financial information contained in this Annual Report has been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union and IFRS as issued by the International Accounting Standards Board (IASB) which vary in certa ...

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

... Timken has entered into individually negotiated contracts with some of its customers. These contracts may extend for one or more years and, if a price is fixed for any period extending beyond current shipments, customarily include a commitment by the customer to purchase a designated percentage of i ...

... Timken has entered into individually negotiated contracts with some of its customers. These contracts may extend for one or more years and, if a price is fixed for any period extending beyond current shipments, customarily include a commitment by the customer to purchase a designated percentage of i ...

Returns to Buying Earnings and Book Value: Accounting for Growth

... application of conservative accounting shifts earnings from the short-term earnings to the long-term. The effects are simply by construction of the accounting. However, these papers are modeled with a fixed discount rate, unrelated to the accounting, so do not deal with the issue of how conservative ...

... application of conservative accounting shifts earnings from the short-term earnings to the long-term. The effects are simply by construction of the accounting. However, these papers are modeled with a fixed discount rate, unrelated to the accounting, so do not deal with the issue of how conservative ...

Annual Report - Primero Mining Corp.

... with the possibility of drilling as deep as 1,500 metres. ...

... with the possibility of drilling as deep as 1,500 metres. ...

Essilor (EI FP)-Buy: Bigger playing field becomes reality

... to meet its +4.5% sales growth at constant FX and perimeter target in FY2015. We forecast +4.6% for FY15e and +5% in Q3 15e due on 22 October. The optical market is still significantly underpenetrated. The “Growing in a Bigger Playing Field” strategy presented by Essilor at its June 2014 Investor Da ...

... to meet its +4.5% sales growth at constant FX and perimeter target in FY2015. We forecast +4.6% for FY15e and +5% in Q3 15e due on 22 October. The optical market is still significantly underpenetrated. The “Growing in a Bigger Playing Field” strategy presented by Essilor at its June 2014 Investor Da ...

Whither Delaware? Limited Commitment and the Financial Value of

... long-term in nature. Second, we consider whether the firm has any large customers, i.e., at least one customer accounting for 10% or more of its sales, which we use as a proxy for the importance of (long-term) firm customers in creating financial value (as in Johnson, Karpoff, and ...

... long-term in nature. Second, we consider whether the firm has any large customers, i.e., at least one customer accounting for 10% or more of its sales, which we use as a proxy for the importance of (long-term) firm customers in creating financial value (as in Johnson, Karpoff, and ...

Libby Libby Short - McGraw Hill Higher Education

... For the year ended June 30, 2001 (in thousands of dollars) Cash provided by (used in): ...

... For the year ended June 30, 2001 (in thousands of dollars) Cash provided by (used in): ...

Chapter 6.

... based on control and influence.2 The definition of direct investment is the same as in the fourth edition of the OECD Benchmark Definition of Foreign Direct Investment, which provides additional details on the FDIR and the collection of direct investment data. Appendix 6a, Topical Summary—Direct Inv ...

... based on control and influence.2 The definition of direct investment is the same as in the fourth edition of the OECD Benchmark Definition of Foreign Direct Investment, which provides additional details on the FDIR and the collection of direct investment data. Appendix 6a, Topical Summary—Direct Inv ...

cash flows

... Developing the Statement of Cash Flows: Classifying Inflows and Outflows of Cash The statement of cash flows essentially summarizes the inflows and outflows of cash during a given period as shown in the following slide (Table 3.3) 1- Decrease/increase in any asset: (difficult for many to grasp (foc ...

... Developing the Statement of Cash Flows: Classifying Inflows and Outflows of Cash The statement of cash flows essentially summarizes the inflows and outflows of cash during a given period as shown in the following slide (Table 3.3) 1- Decrease/increase in any asset: (difficult for many to grasp (foc ...

Form 20-F/A - MOL Corporate

... the non-controlling interest of our subsidiary, Klon Ödeme ve Iletisim Teknolojileri Anonim Şirketi (“PayByMe”). A review of the application of IFRS to options (the “Put Options”) granted by our wholly-owned subsidiary, MOL AccessPortal Sdn. Bhd.(“MOLAP”), in connection with the acquisition by MOLAP ...

... the non-controlling interest of our subsidiary, Klon Ödeme ve Iletisim Teknolojileri Anonim Şirketi (“PayByMe”). A review of the application of IFRS to options (the “Put Options”) granted by our wholly-owned subsidiary, MOL AccessPortal Sdn. Bhd.(“MOLAP”), in connection with the acquisition by MOLAP ...

building today, for tomorrow - EZRA HOLDINGS LIMITED

... • secure diversified funding sources from both financial institutions and capital markets as MLT grows in size; • optimise its cost of debt financing; and • manage the exposure arising from adverse market movements in interest rates and foreign exchange through appropriate hedging strategies. The ...

... • secure diversified funding sources from both financial institutions and capital markets as MLT grows in size; • optimise its cost of debt financing; and • manage the exposure arising from adverse market movements in interest rates and foreign exchange through appropriate hedging strategies. The ...

IFRS Update July 2016

... The amendments address three issues that have arisen in applying the investment entities exception under IFRS 10 Consolidated Financial Statements. The amendments to IFRS 10 clarify that the exemption in paragraph 4 of IFRS 10 from presenting consolidated financial statements applies to a parent ent ...

... The amendments address three issues that have arisen in applying the investment entities exception under IFRS 10 Consolidated Financial Statements. The amendments to IFRS 10 clarify that the exemption in paragraph 4 of IFRS 10 from presenting consolidated financial statements applies to a parent ent ...

RPM by the Numbers

... underlying economic conditions, which is a real testament to our European colleagues, in terms of both their agility and their focus. With RPM’s sales divided between our industrial and consumer businesses, this balanced business model has served us well over the years, with one segment often showin ...

... underlying economic conditions, which is a real testament to our European colleagues, in terms of both their agility and their focus. With RPM’s sales divided between our industrial and consumer businesses, this balanced business model has served us well over the years, with one segment often showin ...

words - Investor Relations Solutions

... Operations” and elsewhere in this Form 10-K may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and as such may involve known and unknown risk, uncertainties and other factors which may cause the actual results, performance or achiev ...

... Operations” and elsewhere in this Form 10-K may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and as such may involve known and unknown risk, uncertainties and other factors which may cause the actual results, performance or achiev ...