What is Situation Ethics?

... moral principles – it worked as it did lead people back to Christianity • It follows one principle so is easy to remember and apply unlike other forms of ethical decision making • It is valuable as it counter acts problems caused by rigidly following laws – e.g. puts people first (personalism) Howev ...

... moral principles – it worked as it did lead people back to Christianity • It follows one principle so is easy to remember and apply unlike other forms of ethical decision making • It is valuable as it counter acts problems caused by rigidly following laws – e.g. puts people first (personalism) Howev ...

Situation Ethics Revision pp

... moral principles – it worked as it did lead people back to Christianity • It follows one principle so is easy to remember and apply unlike other forms of ethical decision making • It is valuable as it counter acts problems caused by rigidly following laws – e.g. puts people first (personalism) Howev ...

... moral principles – it worked as it did lead people back to Christianity • It follows one principle so is easy to remember and apply unlike other forms of ethical decision making • It is valuable as it counter acts problems caused by rigidly following laws – e.g. puts people first (personalism) Howev ...

Center for ETHICS - University of Idaho

... Amoral - not dealing with moral issues... outside the realm of morality. Immoral - Knows right, chooses to do wrong for own benefit... PEP 570, Ethics and the Profession Dr. Stoll,Director and Professor ...

... Amoral - not dealing with moral issues... outside the realm of morality. Immoral - Knows right, chooses to do wrong for own benefit... PEP 570, Ethics and the Profession Dr. Stoll,Director and Professor ...

Fighting Fair – A Call to Ethical Arms

... head, and a band round his neck, do for a guinea what, without these appendages, he would think it wicked and infamous to do for an empire.” Trite though this admonition may sound today, the principle still justifiably haunts contemporary debate around the substance and strictures of legal ethics. I ...

... head, and a band round his neck, do for a guinea what, without these appendages, he would think it wicked and infamous to do for an empire.” Trite though this admonition may sound today, the principle still justifiably haunts contemporary debate around the substance and strictures of legal ethics. I ...

The History Of BioMedical Ethics

... is learnt, ‘at the coalface’, through meeting patients and their families, being involved in their cases. It is a practical discipline. The doctor must learn to recognise the ethical aspects of his/her clinical (and scientific research work), and to make reasoned decisions about this work within the ...

... is learnt, ‘at the coalface’, through meeting patients and their families, being involved in their cases. It is a practical discipline. The doctor must learn to recognise the ethical aspects of his/her clinical (and scientific research work), and to make reasoned decisions about this work within the ...

Ch. 4: Deontology

... as means to my ends). o My rights establish your duties and my rights are the same as the rights of others. ...

... as means to my ends). o My rights establish your duties and my rights are the same as the rights of others. ...

Accounting and Neoliberalism: A Critical - Research Online

... On 28 September 2010, the International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB) released their Conceptual Framework for Financial Reporting 2010 (hereinafter called Framework 2010). This is planned as the first phase of their joint project to develop ...

... On 28 September 2010, the International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB) released their Conceptual Framework for Financial Reporting 2010 (hereinafter called Framework 2010). This is planned as the first phase of their joint project to develop ...

GAAP

... Moreover, the subjective judgments of senior management, accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could ...

... Moreover, the subjective judgments of senior management, accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could ...

information ethics in the knowledge society

... Information ethics and computer ethics are that branch of applied ethics which studies and applied such serial and ethics impacts of ICT. Computer ethics has been used to refer to kind of professionals apply codes of ethics and standards of good practice within their profession. Cyber ethics and int ...

... Information ethics and computer ethics are that branch of applied ethics which studies and applied such serial and ethics impacts of ICT. Computer ethics has been used to refer to kind of professionals apply codes of ethics and standards of good practice within their profession. Cyber ethics and int ...

Credit Union Fraud & Ethics

... process • The most important outcome is achieving desired behaviors • The best way to handle ethics problems is to avoid their occurrence in the first place • Make ethics decision in groups and publicize them, as appropriate www.loescherandassociates.com ...

... process • The most important outcome is achieving desired behaviors • The best way to handle ethics problems is to avoid their occurrence in the first place • Make ethics decision in groups and publicize them, as appropriate www.loescherandassociates.com ...

Kantian Ethics

... because of our nature. This may be a result of our genes or upbringing and so are reactions we cannot control. These acts should not be praised (p.22). ...

... because of our nature. This may be a result of our genes or upbringing and so are reactions we cannot control. These acts should not be praised (p.22). ...

Adjusting Entries

... • Entries made to adjust or update accounts at the end of the accounting period • Required because the trial balance may not contain complete and up-to-date data – Some items are not recorded daily – Some costs are not recorded during the accounting period, as they expire due to the passage of time ...

... • Entries made to adjust or update accounts at the end of the accounting period • Required because the trial balance may not contain complete and up-to-date data – Some items are not recorded daily – Some costs are not recorded during the accounting period, as they expire due to the passage of time ...

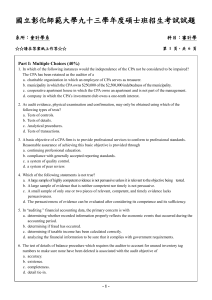

Part II. Essay Questions (60%)

... c. A small sample of only one or two pieces of relevant, competent, and timely evidence lacks persuasiveness. d. The persuasiveness of evidence can be evaluated after considering its competence and its sufficiency. 5. In “auditing ” financial accounting data, the primary concern is with a. determini ...

... c. A small sample of only one or two pieces of relevant, competent, and timely evidence lacks persuasiveness. d. The persuasiveness of evidence can be evaluated after considering its competence and its sufficiency. 5. In “auditing ” financial accounting data, the primary concern is with a. determini ...

Glossary of Ethics - Lonergan Resource

... is most strongly associated with Immanuel Kant, for whom it meant the ability to give the moral law to oneself. It is usually contrasted with "heteronomy" meaning the rule by other sources besides one’s self. To believe people are autonomous is a position opposed to Determinism Blame. An identificat ...

... is most strongly associated with Immanuel Kant, for whom it meant the ability to give the moral law to oneself. It is usually contrasted with "heteronomy" meaning the rule by other sources besides one’s self. To believe people are autonomous is a position opposed to Determinism Blame. An identificat ...

The Ethics Toolkit For Coaches and Mentors

... A contact is a written or verbal agreement between two or more parties that is intended to be enforceable by law. To be legal a contract must begin with a definite offer and a subsequent acceptance of that offer. It must also contain a ‘consideration’ being a benefit which must be bargained for ...

... A contact is a written or verbal agreement between two or more parties that is intended to be enforceable by law. To be legal a contract must begin with a definite offer and a subsequent acceptance of that offer. It must also contain a ‘consideration’ being a benefit which must be bargained for ...

10710 Accounting Eng 30 6 16 - Gauteng Department of Education

... We have audited the annual financial statements of Protea Limited for the year ended 29 February 2016. These financial statements are the responsibility of the company's directors. Basis for Disclaimer of Opinion During the course of our audit we have established that the valuation of fixed assets a ...

... We have audited the annual financial statements of Protea Limited for the year ended 29 February 2016. These financial statements are the responsibility of the company's directors. Basis for Disclaimer of Opinion During the course of our audit we have established that the valuation of fixed assets a ...

2. IntroEthics

... Explanations must be public so that they can be debated and understood by others. ...

... Explanations must be public so that they can be debated and understood by others. ...

presentation

... society as a whole have their attitude toward the actions of the subjects constituting these groups, determined by the dominating values It is due to these values that some actions receive social approval while others do not. Approved actions are those that serve good as defined on the grounds of th ...

... society as a whole have their attitude toward the actions of the subjects constituting these groups, determined by the dominating values It is due to these values that some actions receive social approval while others do not. Approved actions are those that serve good as defined on the grounds of th ...

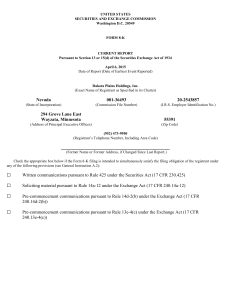

DAKOTA PLAINS HOLDINGS, INC. (Form: 8

... (a) On April 6, 2015, BDO USA, LLP (“BDO”) informed Dakota Plains Holdings, Inc. (the “Company”) of its intention to decline to stand for re-election as the Company’s independent registered accounting firm for the fiscal year ending December 31, 2015. BDO’s reports on the Company’s consolidated fina ...

... (a) On April 6, 2015, BDO USA, LLP (“BDO”) informed Dakota Plains Holdings, Inc. (the “Company”) of its intention to decline to stand for re-election as the Company’s independent registered accounting firm for the fiscal year ending December 31, 2015. BDO’s reports on the Company’s consolidated fina ...

Computerised Accounting System

... Accounting, by definition, is the process of identifying, recording, classifying and summarising financial transactions to produce the financial reports for their ultimate analysis. Let us understand these activities in the context of manual and computerised accounting system. • Identifying : The id ...

... Accounting, by definition, is the process of identifying, recording, classifying and summarising financial transactions to produce the financial reports for their ultimate analysis. Let us understand these activities in the context of manual and computerised accounting system. • Identifying : The id ...

CHAPTER 4 Outline

... Study Objective 4 - Prepare Adjusting Entries for Prepayments Prepayments fall into two categories--prepaid expenses and unearned revenues. Prepaid expenses - expenses paid in cash and recorded as assets until they are used or consumed. Prepaid expenses expire with the passage of time (i. e. rent ...

... Study Objective 4 - Prepare Adjusting Entries for Prepayments Prepayments fall into two categories--prepaid expenses and unearned revenues. Prepaid expenses - expenses paid in cash and recorded as assets until they are used or consumed. Prepaid expenses expire with the passage of time (i. e. rent ...

Chapter 4 – Social And Ethical Responsibility

... norms. But the profit motive and the competitiveness fostered in the free enterprise economic systems put pressure on managers. Learning how to recognise and resolve ethical issues is a crucial step in evaluating ethical decisions in management. It is important to realize that ethics goes beyond leg ...

... norms. But the profit motive and the competitiveness fostered in the free enterprise economic systems put pressure on managers. Learning how to recognise and resolve ethical issues is a crucial step in evaluating ethical decisions in management. It is important to realize that ethics goes beyond leg ...

Accounting ethics

Accounting ethics is primarily a field of applied ethics and is part of business ethics and human ethics, the study of moral values and judgments as they apply to accountancy. It is an example of professional ethics. Accounting introduced by Luca Pacioli, and later expanded by government groups, professional organizations, and independent companies. Ethics are taught in accounting courses at higher education institutions as well as by companies training accountants and auditors.Due to the diverse range of accounting services and recent corporate collapses, attention has been drawn to ethical standards accepted within the accounting profession. These collapses have resulted in a widespread disregard for the reputation of the accounting profession. To combat the criticism and prevent fraudulent accounting, various accounting organizations and governments have developed regulations and remedies for improved ethics among the accounting profession.