Institutional Presence - American Economic Association

... Kim (2010) find that institutional investors benefit from geographical proximity to local stocks, potentially due to proximity facilitating information collection of companies. Yet, it is unclear whether this proximity is mutually beneficial for companies located close to institutional investors. Th ...

... Kim (2010) find that institutional investors benefit from geographical proximity to local stocks, potentially due to proximity facilitating information collection of companies. Yet, it is unclear whether this proximity is mutually beneficial for companies located close to institutional investors. Th ...

Arbitrage Opportunities

... in the FX market is an example of perfect substitutes with convertibility and is not affected by these traditional impediments to arbitrage We explicitly model the process by which arbitrageurs trade upon observing a violation of an arbitrage parity. Each arbitrageur maximizes her trading profits, ...

... in the FX market is an example of perfect substitutes with convertibility and is not affected by these traditional impediments to arbitrage We explicitly model the process by which arbitrageurs trade upon observing a violation of an arbitrage parity. Each arbitrageur maximizes her trading profits, ...

Default Option Exercise over the Financial Crisis and Beyond

... Elul et al, 2010; Campell and Cocco, 2015). Rolling window hazard model estimates show marked run-up in the negative equity beta from 0.13 in 2007 to 0.80 in 2012 (Figure 1), translating into substantially higher default probabilities for a given level of negative equity. For example, in 2007, a mor ...

... Elul et al, 2010; Campell and Cocco, 2015). Rolling window hazard model estimates show marked run-up in the negative equity beta from 0.13 in 2007 to 0.80 in 2012 (Figure 1), translating into substantially higher default probabilities for a given level of negative equity. For example, in 2007, a mor ...

Enron: Corporate Failure, Market Success

... All firms face agency problems, and in the process of running a going concern develop measures to control them. Such measures include controls on the actions of agents, monitoring the actions of agents, financial incentives to encourage agents to act in the interests of the principals, and the separ ...

... All firms face agency problems, and in the process of running a going concern develop measures to control them. Such measures include controls on the actions of agents, monitoring the actions of agents, financial incentives to encourage agents to act in the interests of the principals, and the separ ...

Managerial Risk-Taking and CEO Excess Compensation

... the firm (Guay, 1999; HabibandLjungqvist, 2005).The negative effect of higher delta and vegais that they expose CEOs to incentive risk. CEOs are less diversified with respect to firm-specific wealth than are diversified shareholders because stocks and optionsreceived by CEOs as part of their compens ...

... the firm (Guay, 1999; HabibandLjungqvist, 2005).The negative effect of higher delta and vegais that they expose CEOs to incentive risk. CEOs are less diversified with respect to firm-specific wealth than are diversified shareholders because stocks and optionsreceived by CEOs as part of their compens ...

Evidence of the Abnormal Accrual Anomaly Incremental to

... with returns from random size-matched portfolios. The first two tests are proposed by Bernard et al. (1997). First, they suggest that if anomalous results occur due to investor mispricing and this mispricing relates to an earnings-based anomaly, then abnormal returns should concentrate around future ...

... with returns from random size-matched portfolios. The first two tests are proposed by Bernard et al. (1997). First, they suggest that if anomalous results occur due to investor mispricing and this mispricing relates to an earnings-based anomaly, then abnormal returns should concentrate around future ...

Mutual Funds and Bubbles: The Surprising Role of Contractual

... However, the seemingly irrational behavior described above is not a characteristic of the entire fund-management industry. There still were many managers who followed a contrarian strategy or at least held a cautious/prudent view toward the rising stock market.1 In this article, we focus on a twofol ...

... However, the seemingly irrational behavior described above is not a characteristic of the entire fund-management industry. There still were many managers who followed a contrarian strategy or at least held a cautious/prudent view toward the rising stock market.1 In this article, we focus on a twofol ...

CPB Discussion Paper

... The equity premium is a key parameter in asset allocation policies. It measures the excess return above the risk-free return and as such it can be seen as the price for risk. There has been a lively debate in the theoretical as well as the empirical literature on the measurement, size and sources of ...

... The equity premium is a key parameter in asset allocation policies. It measures the excess return above the risk-free return and as such it can be seen as the price for risk. There has been a lively debate in the theoretical as well as the empirical literature on the measurement, size and sources of ...

More Finance Questions

... a. the pain that Rob would experience if he lost $200 of his wealth would exceed the pleasure that he would experience if he added $200 to his wealth. b. the pleasure that Rob would experience if he added $200 to his wealth would exceed the pain that he would experience if he lost $200 of his wealth ...

... a. the pain that Rob would experience if he lost $200 of his wealth would exceed the pleasure that he would experience if he added $200 to his wealth. b. the pleasure that Rob would experience if he added $200 to his wealth would exceed the pain that he would experience if he lost $200 of his wealth ...

Essays on Trading Strategies and Long Memory

... submitted and approved for the award of a degree by this or any other University. Signature: ...

... submitted and approved for the award of a degree by this or any other University. Signature: ...

Key Issues in the CLO Market Today

... Recently, some non-call and reinvestment periods have become longer ...

... Recently, some non-call and reinvestment periods have become longer ...

The concept of investment efficiency and its application to

... - greater confidence for allocation to new asset classes/structures; and - investment policies that are more aligned with a fund's risk/reward tolerance. 2.5.6 This process is likely to provide fiduciaries with a better understanding of their fund. This should enhance choices made regarding fund obj ...

... - greater confidence for allocation to new asset classes/structures; and - investment policies that are more aligned with a fund's risk/reward tolerance. 2.5.6 This process is likely to provide fiduciaries with a better understanding of their fund. This should enhance choices made regarding fund obj ...

Lyxor Index Fund December 2014

... States Investment Company Act of 1940, as amended (the “Investment Company Act”). Based on interpretations of the Investment Company Act by the staff of the United States Securities and Exchange Commission (the “SEC”) relating to foreign investment companies, if the Company has more than one hundred ...

... States Investment Company Act of 1940, as amended (the “Investment Company Act”). Based on interpretations of the Investment Company Act by the staff of the United States Securities and Exchange Commission (the “SEC”) relating to foreign investment companies, if the Company has more than one hundred ...

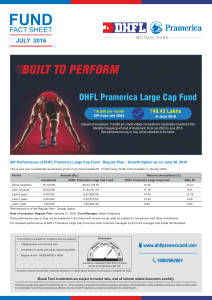

DHFL Pramerica Large Cap Fund

... Regular Plan and Direct Plan are available for subscription as per the below details Inception Date: Regular Plan: 21/01/2003, Direct Plan: 01/01/2013. Application Amount: ` 5000/- and in multiples of ` 1/- thereafter. Additional Purchase Amount: ` 1000/- and in multiples of `1/-thereafter or 100 un ...

... Regular Plan and Direct Plan are available for subscription as per the below details Inception Date: Regular Plan: 21/01/2003, Direct Plan: 01/01/2013. Application Amount: ` 5000/- and in multiples of ` 1/- thereafter. Additional Purchase Amount: ` 1000/- and in multiples of `1/-thereafter or 100 un ...

What is the information content of dividend changes

... not about expected increases (decreases) in future cash flow, it may relate to changes in firms’ systematic risks. Based on this recognition, Grullon et al. (2002) present an alternative explanation, the “maturity hypothesis,” to explain the price changes upon dividend change announcement. Specifica ...

... not about expected increases (decreases) in future cash flow, it may relate to changes in firms’ systematic risks. Based on this recognition, Grullon et al. (2002) present an alternative explanation, the “maturity hypothesis,” to explain the price changes upon dividend change announcement. Specifica ...

Cost of capital and earnings transparency

... We predict that earnings transparency is negatively associated with cost of capital. The basis for our prediction is the well-established positive relation between information asymmetry and cost of capital and our expectation that earnings transparency is negatively associated with information asymm ...

... We predict that earnings transparency is negatively associated with cost of capital. The basis for our prediction is the well-established positive relation between information asymmetry and cost of capital and our expectation that earnings transparency is negatively associated with information asymm ...

Belief Heterogeneity, Collateral Constraint, and Asset Prices with a

... equilibria in Kehoe and Levine (2001), in which the authors show that the dynamics of the former is much more complex than the one of the latter. Liquidity constrained economies are special cases of collateral constrained economies when the set of …nancial assets is chosen to be empty. ...

... equilibria in Kehoe and Levine (2001), in which the authors show that the dynamics of the former is much more complex than the one of the latter. Liquidity constrained economies are special cases of collateral constrained economies when the set of …nancial assets is chosen to be empty. ...

Long-Short Commodity Investing - EDHEC

... a well-diversified portfolio does not solely depend on the risk premium of commodity futures viewed as an asset class but is also driven by a desire for risk diversification and thus depends on how the returns of commodity investments correlate with the rest of the investor’s portfolio over time. Th ...

... a well-diversified portfolio does not solely depend on the risk premium of commodity futures viewed as an asset class but is also driven by a desire for risk diversification and thus depends on how the returns of commodity investments correlate with the rest of the investor’s portfolio over time. Th ...

What makes a great value investor?

... Management structure and the re-launch as Kennox. Of the 22 stocks held when the CGAM portfolio was closed in September 2008, 21 were bought to start the Kennox Strategic Value Fund in April 2009. Assuming a static portfolio for the hiatus period allows Kennox to show a continuous performance record ...

... Management structure and the re-launch as Kennox. Of the 22 stocks held when the CGAM portfolio was closed in September 2008, 21 were bought to start the Kennox Strategic Value Fund in April 2009. Assuming a static portfolio for the hiatus period allows Kennox to show a continuous performance record ...

Wealth Distribution with State- dependent Risk Aversion

... from the asset market to labor market and therefore shifts the wealth from the rich to the poor. Thus, although both rich and poor agents’s absolute wealth increases, the percent of wealth held by the rich decreases. Next we introduce the state-dependent risk aversion into this model and assume tha ...

... from the asset market to labor market and therefore shifts the wealth from the rich to the poor. Thus, although both rich and poor agents’s absolute wealth increases, the percent of wealth held by the rich decreases. Next we introduce the state-dependent risk aversion into this model and assume tha ...

strAtegIc FINANcIAL MANAgeMeNt (sFM)

... benefits receivable thereon over the economic life of the asset or project for which investments are made. Estimating cost is relatively easier as it is made in the current period, but estimating benefits is very difficult as it relates to future period involving risk and uncertainty. For estimating ...

... benefits receivable thereon over the economic life of the asset or project for which investments are made. Estimating cost is relatively easier as it is made in the current period, but estimating benefits is very difficult as it relates to future period involving risk and uncertainty. For estimating ...

Standard Bank Group

... include the exposures from our global markets outside Africa operations, which for financial reporting purposes have been separately classified as non-current assets and liabilities held for sale in the comparative period. The group’s controlling interest in Standard Bank Plc, which included the gro ...

... include the exposures from our global markets outside Africa operations, which for financial reporting purposes have been separately classified as non-current assets and liabilities held for sale in the comparative period. The group’s controlling interest in Standard Bank Plc, which included the gro ...

Does Investor Identity Matter in Equity Issues

... of affiliated investors to be more pronounced for non-distressed firms with access to both private and public equity markets. The results indicate that unaffiliated investors purchase shares at significantly deeper discounts than affiliated investors, but we find no significant difference between th ...

... of affiliated investors to be more pronounced for non-distressed firms with access to both private and public equity markets. The results indicate that unaffiliated investors purchase shares at significantly deeper discounts than affiliated investors, but we find no significant difference between th ...

Why Does the Law of One Price Fail?

... investments to shift toward lower-cost index funds relative to control subjects who received only the fund prospectuses. However, over 80% of these fee transparency treatment subjects still fail to minimize index fund fees. In a second treatment, subjects receive the four prospectuses and a summary ...

... investments to shift toward lower-cost index funds relative to control subjects who received only the fund prospectuses. However, over 80% of these fee transparency treatment subjects still fail to minimize index fund fees. In a second treatment, subjects receive the four prospectuses and a summary ...

Download attachment

... scholars and knowledge of Islamic bonds. Netta Thakur (2007) and Julia Berris (2007) point to the many UK companies that have opened Islamic banking and financial brokerage desks in order to create liquidity in the UK Islamic bond market, increase the growth of secondary markets and ensure equality ...

... scholars and knowledge of Islamic bonds. Netta Thakur (2007) and Julia Berris (2007) point to the many UK companies that have opened Islamic banking and financial brokerage desks in order to create liquidity in the UK Islamic bond market, increase the growth of secondary markets and ensure equality ...

Beta (finance)

In finance, the beta (β) of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not go up or down a lot, so it has a low beta. An example of the second is gold. The price of gold does go up and down a lot, but not in the same direction or at the same time as the market.A beta greater than one generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like equity put options can have large negative betas.Beta is important because it measures the risk of an investment that cannot be reduced by diversification. It does not measure the risk of an investment held on a stand-alone basis, but the amount of risk the investment adds to an already-diversified portfolio. In the capital asset pricing model, beta risk is the only kind of risk for which investors should receive an expected return higher than the risk-free rate of interest.The definition above covers only theoretical beta. The term is used in many related ways in finance. For example, the betas commonly quoted in mutual fund analyses generally measure the risk of the fund arising from exposure to a benchmark for the fund, rather than from exposure to the entire market portfolio. Thus they measure the amount of risk the fund adds to a diversified portfolio of funds of the same type, rather than to a portfolio diversified among all fund types.Beta decay refers to the tendency for a company with a high beta coefficient (β > 1) to have its beta coefficient decline to the market beta. It is an example of regression toward the mean.