Non-GAAP Reporting following Debt Covenant Violations

... sustainable core operating performance (Bhattacharya et al., 2003). Recent evidence suggests that the nonGAAP earnings measures used in debt contracts are also created to better measure persistent operating performance. Li (2010) argues that earnings measures in debt contracts are more useful if the ...

... sustainable core operating performance (Bhattacharya et al., 2003). Recent evidence suggests that the nonGAAP earnings measures used in debt contracts are also created to better measure persistent operating performance. Li (2010) argues that earnings measures in debt contracts are more useful if the ...

Does the Dodd-Frank Act Reduce Conflicts of Interest Faced by

... Second, I want to analyze whether and which rating agency is a§ected more by the passage of the law in terms of rating stability. Third, I want to investigate the reputation e§ect of the regulation on both rating agencies. In addition, I want to understand whether ratings a§ect the Örm tendency to r ...

... Second, I want to analyze whether and which rating agency is a§ected more by the passage of the law in terms of rating stability. Third, I want to investigate the reputation e§ect of the regulation on both rating agencies. In addition, I want to understand whether ratings a§ect the Örm tendency to r ...

Subnational Capital Markets in Developing Countries

... This book draws from the findings of the Global Program on Subnational Capital Markets launched in 1998 by the World Bank with the sponsorship of the governments of Austria, Finland, Japan, Spain, Sweden, and Switzerland. Led by Augusto de La Torre, Mila Freire, and Marcela Huertas under the supervi ...

... This book draws from the findings of the Global Program on Subnational Capital Markets launched in 1998 by the World Bank with the sponsorship of the governments of Austria, Finland, Japan, Spain, Sweden, and Switzerland. Led by Augusto de La Torre, Mila Freire, and Marcela Huertas under the supervi ...

Nordic High Yield Update

... There are some positives. Other non-Norwegian sectors such as industrials and consumer goods remain relatively less impacted. Moreover, in line with our argument that industries that benefit from the oil price decline lag those that do not, we continue to have a positive view on the transportation i ...

... There are some positives. Other non-Norwegian sectors such as industrials and consumer goods remain relatively less impacted. Moreover, in line with our argument that industries that benefit from the oil price decline lag those that do not, we continue to have a positive view on the transportation i ...

US CORNER - Paul, Weiss

... lien lenders could have room to stretch their maturity. This is less likely to be the case with a second lien loan where the maturity is typically only six to at most twelve months beyond the first lien debt. Unlike unsecured creditors who were generally on the outside looking in, second lien lender ...

... lien lenders could have room to stretch their maturity. This is less likely to be the case with a second lien loan where the maturity is typically only six to at most twelve months beyond the first lien debt. Unlike unsecured creditors who were generally on the outside looking in, second lien lender ...

Does The Firm Information Environment Influence Financing

... less information sensitive debt financing in the post Reg FD regime. Separately, Wang (2007) notes that Reg FD largely targets firms that rely on selective disclosure. To the extent that this is true, one could argue that Reg FD will have a distinct impact on the financing choices of firms that rel ...

... less information sensitive debt financing in the post Reg FD regime. Separately, Wang (2007) notes that Reg FD largely targets firms that rely on selective disclosure. To the extent that this is true, one could argue that Reg FD will have a distinct impact on the financing choices of firms that rel ...

Liquidity Crises, Liquidity Lines and Sovereign Risk December 2015

... liquidity lines during a liquidity crisis. A defaulting government faces a default cost, is temporarily excluded from the financial markets and cannot issue new debt. Furthermore, a defaulting government cannot rollover its debt accrued from liquidity lines and has to honor these obligations but do ...

... liquidity lines during a liquidity crisis. A defaulting government faces a default cost, is temporarily excluded from the financial markets and cannot issue new debt. Furthermore, a defaulting government cannot rollover its debt accrued from liquidity lines and has to honor these obligations but do ...

unit 7 financial and operating leverage module - 2

... These relationships indicate that both these measures of financial leverage will rank companies in the same order. However, the first measure (i.e. D/V) is more specific as its value will range between zero to one. The value of the second measure (i.e. D/E) may vary from zero to any large number. Th ...

... These relationships indicate that both these measures of financial leverage will rank companies in the same order. However, the first measure (i.e. D/V) is more specific as its value will range between zero to one. The value of the second measure (i.e. D/E) may vary from zero to any large number. Th ...

Accounting Comparability and Loan Contracting - CEAR

... Second, this study contributes to our understanding of the relationship between accounting quality and the cost of capital. The extensive literature examining this relationship in the equity market has not been able to reach a consensus as to whether and how financial reporting quality and the cost ...

... Second, this study contributes to our understanding of the relationship between accounting quality and the cost of capital. The extensive literature examining this relationship in the equity market has not been able to reach a consensus as to whether and how financial reporting quality and the cost ...

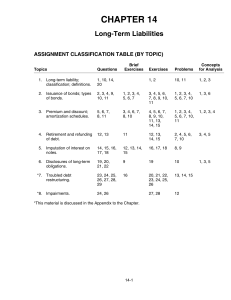

CHAPTER 14 Long-Term Liabilities

... 22. In take-or-pay contracts, the outside party agrees to make specified minimum payments even if it does not take possession of the contracted goods or services. In through-put contracts, the outside party agrees to pay specified amounts in return for processing or transportation services rendered ...

... 22. In take-or-pay contracts, the outside party agrees to make specified minimum payments even if it does not take possession of the contracted goods or services. In through-put contracts, the outside party agrees to pay specified amounts in return for processing or transportation services rendered ...

Capital structure and volatility of risk

... called volatility of implied volatility (VIV). All our results are implemented both of these measures of volatility of volatility. We rank firms in deciles according to our volatility of volatility measures (both VRV and VIV) and we find that the firms in the higher deciles issue monotonically small ...

... called volatility of implied volatility (VIV). All our results are implemented both of these measures of volatility of volatility. We rank firms in deciles according to our volatility of volatility measures (both VRV and VIV) and we find that the firms in the higher deciles issue monotonically small ...

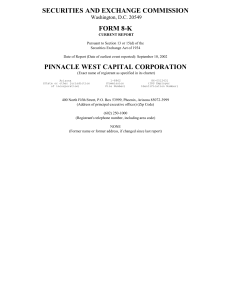

PINNACLE WEST CAPITAL CORP (Form: 8-K

... between APS and PWEC under different regulatory regimes results in PWEC being unable to attain investment grade credit ratings. This, in turn, precludes PWEC from accessing capital markets to refinance the bridge financing provided by the Company to fund the construction of the PWEC Assets or from e ...

... between APS and PWEC under different regulatory regimes results in PWEC being unable to attain investment grade credit ratings. This, in turn, precludes PWEC from accessing capital markets to refinance the bridge financing provided by the Company to fund the construction of the PWEC Assets or from e ...

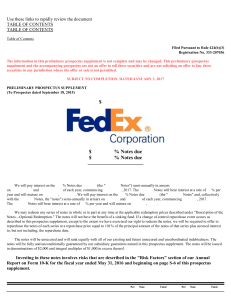

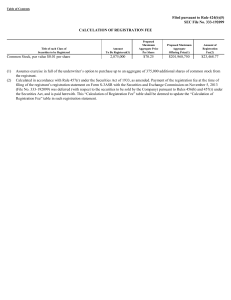

FEDEX CORP (Form: 424B3, Received: 01/03/2017 08:57:53)

... identified under the heading "Risk Factors" in "Management's Discussion and Analysis of Results of Operations and Financial Condition" in our Annual Report on Form 10-K for the fiscal year ended May 31, 2016, (ii) the factors set forth below related to the notes, and (iii) the other information set ...

... identified under the heading "Risk Factors" in "Management's Discussion and Analysis of Results of Operations and Financial Condition" in our Annual Report on Form 10-K for the fiscal year ended May 31, 2016, (ii) the factors set forth below related to the notes, and (iii) the other information set ...

Diamondback Energy, Inc.

... During the six months ended June 30, 2015, our average daily production was approximately 30,302 BOE/d, consisting of 22,894 Bbls/d of oil, 18,795 Mcf/d of natural gas and 4,276 Bbls/d of natural gas liquids, an increase of 14,596 BOE/d, or 93%, from average daily production of 15,706 BOE/d for the ...

... During the six months ended June 30, 2015, our average daily production was approximately 30,302 BOE/d, consisting of 22,894 Bbls/d of oil, 18,795 Mcf/d of natural gas and 4,276 Bbls/d of natural gas liquids, an increase of 14,596 BOE/d, or 93%, from average daily production of 15,706 BOE/d for the ...

Document

... reported. Generally, only accounts receivable is disclosed since the other types of receivables are not material. In some cases, the other types of receivables are disclosed in the notes to the ...

... reported. Generally, only accounts receivable is disclosed since the other types of receivables are not material. In some cases, the other types of receivables are disclosed in the notes to the ...

How and Why Credit Rating Agencies are not Like Other Gatekeepers

... market structure that is reinforced by regulations that depend exclusively on credit ratings issued by Nationally Recognized Statistical Rating Organizations (NRSROs).7 These regulatory benefits – which I call “regulatory licenses” – generate economic rents for NRSROs that persist even when they per ...

... market structure that is reinforced by regulations that depend exclusively on credit ratings issued by Nationally Recognized Statistical Rating Organizations (NRSROs).7 These regulatory benefits – which I call “regulatory licenses” – generate economic rents for NRSROs that persist even when they per ...

Saving Your Home in Bankruptcy

... rental housing. If debtors default but do not file for bankruptcy, then mortgage lenders are assumed to foreclose and debtors relocate to rental housing. Assume that debtors’ relocation cost is L and that rental housing costs R per year. Lenders’ cost of foreclosure is denoted C f . Mortgages are a ...

... rental housing. If debtors default but do not file for bankruptcy, then mortgage lenders are assumed to foreclose and debtors relocate to rental housing. Assume that debtors’ relocation cost is L and that rental housing costs R per year. Lenders’ cost of foreclosure is denoted C f . Mortgages are a ...

as a PDF - Illinois Law Review

... The article also rejects the contention that regulation would mitigate any negative consequences of rating agency misbehavior. Although the practice of requiring issuers to pay for a rating raises a potential conflict of interest, Professor Schwarcz argues that the risk of misbehavior is minimal and ...

... The article also rejects the contention that regulation would mitigate any negative consequences of rating agency misbehavior. Although the practice of requiring issuers to pay for a rating raises a potential conflict of interest, Professor Schwarcz argues that the risk of misbehavior is minimal and ...

- UConn School of Business

... expense of the owners. Building on this concept, the theoretical literature has identified a variety of incentives that can lead managers to deviate from policies that maximize shareholder value. For example, undiversified wealth and human capital invested in the firm may lead risk-averse managers ...

... expense of the owners. Building on this concept, the theoretical literature has identified a variety of incentives that can lead managers to deviate from policies that maximize shareholder value. For example, undiversified wealth and human capital invested in the firm may lead risk-averse managers ...

The Gains from Resolving Debt Overhang: Evidence from a

... firm realizes its investment opportunities and its initial level of productivity. The firm then makes an initial debt decision in the face of a classical trade-off to maximize the joint value of equity holders and new creditors. Firms take out debt because it has a tax advantage, but do not fully fi ...

... firm realizes its investment opportunities and its initial level of productivity. The firm then makes an initial debt decision in the face of a classical trade-off to maximize the joint value of equity holders and new creditors. Firms take out debt because it has a tax advantage, but do not fully fi ...

The Interplay Between Student Loans and Credit Cards: Implications for Default ∗

... (2009)). While both of these loans represent important components of young households’ portfolios in the U.S., the financial arrangements in the two markets are very different, and in particular with respect to the roles played by bankruptcy arrangements and default pricing. Furthermore, credit term ...

... (2009)). While both of these loans represent important components of young households’ portfolios in the U.S., the financial arrangements in the two markets are very different, and in particular with respect to the roles played by bankruptcy arrangements and default pricing. Furthermore, credit term ...

Small Firm Use of Debt: An Examination of the Smallest Small Firms

... address a broad range of needs: to cover start-up costs, to provide working capital, to secure facilities or equipment, and to hire employees. Most small firms are at a relative disadvantage, because they are too small to access the public debt and equity markets. Similarly, they are typically too s ...

... address a broad range of needs: to cover start-up costs, to provide working capital, to secure facilities or equipment, and to hire employees. Most small firms are at a relative disadvantage, because they are too small to access the public debt and equity markets. Similarly, they are typically too s ...

DBRS Recovery Ratings for Non-Investment Grade

... or maintenance capital expenditures) is one early warning sign of potential default. In other cases, consideration might be appropriate for situations where an issuer may pre-emptively file for bankruptcy protection in order to reorganize its capital structure or gain concessions from labour, suppli ...

... or maintenance capital expenditures) is one early warning sign of potential default. In other cases, consideration might be appropriate for situations where an issuer may pre-emptively file for bankruptcy protection in order to reorganize its capital structure or gain concessions from labour, suppli ...

Debt Refinancing and Equity Returns∗

... which could matter for the extent to which shareholders care about their firm’s debt refinancing risk. Specifically, we add proxies for firms’ cash holdings, profitability, and other variables used in the literature on financial constraints. Overall, this paper provides new insights for the cross-se ...

... which could matter for the extent to which shareholders care about their firm’s debt refinancing risk. Specifically, we add proxies for firms’ cash holdings, profitability, and other variables used in the literature on financial constraints. Overall, this paper provides new insights for the cross-se ...