Efficient or Inefficient Markets: A Behavioral Finance Perspective

... As more and more researches tested EMH, some rather controversial evidence began to appear. An unexpected blow came in 1980 in the form of Grossman Stiglitz paradox; published in their article in 1980 “On the impossibility of informationally efficient markets” They argued that if all relevant inform ...

... As more and more researches tested EMH, some rather controversial evidence began to appear. An unexpected blow came in 1980 in the form of Grossman Stiglitz paradox; published in their article in 1980 “On the impossibility of informationally efficient markets” They argued that if all relevant inform ...

Lower Middle Market Direct Lending

... Collectively, direct lenders addressing the lower middle market and middle market can deliver a compelling yield opportunity to investors driven largely by the macro trend of bank consolidation against the backdrop of tremendous capital demand. Lower middle market and middle market direct lending st ...

... Collectively, direct lenders addressing the lower middle market and middle market can deliver a compelling yield opportunity to investors driven largely by the macro trend of bank consolidation against the backdrop of tremendous capital demand. Lower middle market and middle market direct lending st ...

s - Research Portal

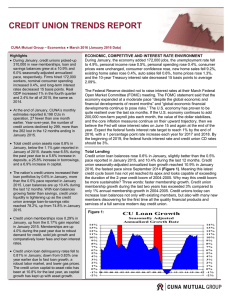

... (chart 2). A recovery in property prices and the boost to real wages from low inflation have helped spur a sharp rise in consumer sentiment back to pre-recession levels (chart 3). Although latest data show a surge in investment which is the product of volatile factors, underlying investment demand a ...

... (chart 2). A recovery in property prices and the boost to real wages from low inflation have helped spur a sharp rise in consumer sentiment back to pre-recession levels (chart 3). Although latest data show a surge in investment which is the product of volatile factors, underlying investment demand a ...

What Is Stock

... 3. The Federal Reserve Open Market Committee judges that some further policy firming might be needed to address inflation risks. ...

... 3. The Federal Reserve Open Market Committee judges that some further policy firming might be needed to address inflation risks. ...

EN EN Results of in-depth reviews under Regulation (EU) No 1176

... regulations; the global economic and financial crisis hampered the ability of Dutch banks to borrow in wholesale markets. Given the importance of securitised funding, this pushed up domestic lending rates especially for housing finance. New EU banking regulations underscore the importance of larger ...

... regulations; the global economic and financial crisis hampered the ability of Dutch banks to borrow in wholesale markets. Given the importance of securitised funding, this pushed up domestic lending rates especially for housing finance. New EU banking regulations underscore the importance of larger ...

3. What determines the yields for treasury bills in Pakistan.

... of different denominations are floated fortnightly by SBP and rates are offered to investors who bid and buy them SBP, (2008). Little work seems to have addressed the determination of yields of treasury bills in Pakistan. There could be many plausible factors that determine these yields in the indig ...

... of different denominations are floated fortnightly by SBP and rates are offered to investors who bid and buy them SBP, (2008). Little work seems to have addressed the determination of yields of treasury bills in Pakistan. There could be many plausible factors that determine these yields in the indig ...

Complete Transcript

... have? Well firstly they have that right to redeem. As I have said, the right to redeem is the right to pay off the debt and to take the property back free from the mortgage and the lender's rights. Although the 1925 Act altered how a mortgage could be made, it did not alter the borrower's right to r ...

... have? Well firstly they have that right to redeem. As I have said, the right to redeem is the right to pay off the debt and to take the property back free from the mortgage and the lender's rights. Although the 1925 Act altered how a mortgage could be made, it did not alter the borrower's right to r ...

Economic and Strategy Viewpoint - January 2016

... the back of the Hong Kong Shanghai connect found new legs in March as expectations of stimulus built and the government first implicitly and then explicitly endorsed the boom in equities. Convinced of government support for the market, investors piled in, with the index 60% higher by June than at th ...

... the back of the Hong Kong Shanghai connect found new legs in March as expectations of stimulus built and the government first implicitly and then explicitly endorsed the boom in equities. Convinced of government support for the market, investors piled in, with the index 60% higher by June than at th ...

3.1. Housing market and household sector indebtedness

... Macroeconomic risks related to high indebtedness of the private sector continue to be important, despite a number of mitigating factors and recently introduced policy measures on housing and corporate taxation. Corporate debt has declined substantially since 2009 but remains high even if the large b ...

... Macroeconomic risks related to high indebtedness of the private sector continue to be important, despite a number of mitigating factors and recently introduced policy measures on housing and corporate taxation. Corporate debt has declined substantially since 2009 but remains high even if the large b ...

United States housing bubble

The United States housing bubble was an economic bubble affecting many parts of the United States housing market in over half of American states. Housing prices peaked in early 2006, started to decline in 2006 and 2007, and reached new lows in 2012. On December 30, 2008, the Case-Shiller home price index reported its largest price drop in its history. The credit crisis resulting from the bursting of the housing bubble is—according to general consensus—the primary cause of the 2007–2009 recession in the United States.Increased foreclosure rates in 2006–2007 among U.S. homeowners led to a crisis in August 2008 for the subprime, Alt-A, collateralized debt obligation (CDO), mortgage, credit, hedge fund, and foreign bank markets. In October 2007, the U.S. Secretary of the Treasury called the bursting housing bubble ""the most significant risk to our economy.""Any collapse of the U.S. housing bubble has a direct impact not only on home valuations, but the nation's mortgage markets, home builders, real estate, home supply retail outlets, Wall Street hedge funds held by large institutional investors, and foreign banks, increasing the risk of a nationwide recession. Concerns about the impact of the collapsing housing and credit markets on the larger U.S. economy caused President George W. Bush and the Chairman of the Federal Reserve Ben Bernanke to announce a limited bailout of the U.S. housing market for homeowners who were unable to pay their mortgage debts.In 2008 alone, the United States government allocated over $900 billion to special loans and rescues related to the U.S. housing bubble, with over half going to Fannie Mae and Freddie Mac (both of which are government-sponsored enterprises) as well as the Federal Housing Administration. On December 24, 2009, the Treasury Department made an unprecedented announcement that it would be providing Fannie Mae and Freddie Mac unlimited financial support for the next three years despite acknowledging losses in excess of $400 billion so far. The Treasury has been criticized for encroaching on spending powers that are enumerated for Congress alone by the United States Constitution, and for violating limits imposed by the Housing and Economic Recovery Act of 2008.