PDPE Market Analysis Tool: Price and Income Elasticities

... is inelastic. If the quantity demanded responds equally to changes in price or income, demand is unit elastic. Three types of elasticities are important in market analysis, namely the own-price elasticity, the income elasticity and the cross-price elasticities. A (own-)price elasticity is defined a ...

... is inelastic. If the quantity demanded responds equally to changes in price or income, demand is unit elastic. Three types of elasticities are important in market analysis, namely the own-price elasticity, the income elasticity and the cross-price elasticities. A (own-)price elasticity is defined a ...

Elasticity

... the y-axis variable) over the run (difference in the x-axis variable.) Think of an elasticity as a slope on steroids. 14. When we talk about supply and demand the elasticity is always about quantity with respect to price. When the quantity is on the x-axis, the elasticity is the change in quantity w ...

... the y-axis variable) over the run (difference in the x-axis variable.) Think of an elasticity as a slope on steroids. 14. When we talk about supply and demand the elasticity is always about quantity with respect to price. When the quantity is on the x-axis, the elasticity is the change in quantity w ...

chap011imEDIT

... A. Consumer choice and the budget constraint: 1. Consumers are assumed to be rational, i.e. they are trying to get the most value for their money. 2. Consumers have clear-cut preferences for various goods and services and can judge the utility they receive from successive units of various purchases. ...

... A. Consumer choice and the budget constraint: 1. Consumers are assumed to be rational, i.e. they are trying to get the most value for their money. 2. Consumers have clear-cut preferences for various goods and services and can judge the utility they receive from successive units of various purchases. ...

Economics Of Business And Finance BA ECONOMICS 275

... cost can be measured in terms of the interest he would have earned by lending that money to somebody. Similarly, when he devotes his time in organising his business, the opportunity cost may be measured in terms of the salaries he would have earned from some employment elsewhere. (3)Marginal Analysi ...

... cost can be measured in terms of the interest he would have earned by lending that money to somebody. Similarly, when he devotes his time in organising his business, the opportunity cost may be measured in terms of the salaries he would have earned from some employment elsewhere. (3)Marginal Analysi ...

Taxes and Welfare

... levels for which marginal social benefit equals marginal social cost. (MSB = MSC) ...

... levels for which marginal social benefit equals marginal social cost. (MSB = MSC) ...

Chapter 6 INFLATION

... level increases from P0 to P1, ⇒ real wage rate has decreased and unemployment falls below its natural rate (above FE) ⇒ there is a shortage of labor ⇒ money wage rate starts to increase to attract more labor ⇒ SAS starts to decrease ⇒ SAS curve starts to shift leftward ⇒ P starts to increase and RG ...

... level increases from P0 to P1, ⇒ real wage rate has decreased and unemployment falls below its natural rate (above FE) ⇒ there is a shortage of labor ⇒ money wage rate starts to increase to attract more labor ⇒ SAS starts to decrease ⇒ SAS curve starts to shift leftward ⇒ P starts to increase and RG ...

Chapter 7 - Powerpoint

... The diamond-water paradox refers to the puzzling observation that markets place a very high value on diamonds at the same time that water is cheap. However, in reality there is no paradox of value. P ...

... The diamond-water paradox refers to the puzzling observation that markets place a very high value on diamonds at the same time that water is cheap. However, in reality there is no paradox of value. P ...

lecture notes

... A. Consumer choice and the budget constraint: 1. Consumers are assumed to be rational, i.e. they are trying to get the most value for their money. 2. Consumers have clear-cut preferences for various goods and services and can judge the utility they receive from successive units of various purchases. ...

... A. Consumer choice and the budget constraint: 1. Consumers are assumed to be rational, i.e. they are trying to get the most value for their money. 2. Consumers have clear-cut preferences for various goods and services and can judge the utility they receive from successive units of various purchases. ...

Supply And Demand

... The law of supply is accounted for by two factors: In the face of rising prices, firms arrange their activities to supply more of the good to the market, substituting production of that good for the production of other goods. Assuming firms' costs are constant, a higher price means ...

... The law of supply is accounted for by two factors: In the face of rising prices, firms arrange their activities to supply more of the good to the market, substituting production of that good for the production of other goods. Assuming firms' costs are constant, a higher price means ...

Entry - Unito

... incumbent and potential entrant that the optimal first period price for a low cost incumbent is different from that of a high cost incumbent. For a high cost incumbent, that price is its unconstrained monopoly price, accepting, that entry will occur in the second period. But for the low cost incumbe ...

... incumbent and potential entrant that the optimal first period price for a low cost incumbent is different from that of a high cost incumbent. For a high cost incumbent, that price is its unconstrained monopoly price, accepting, that entry will occur in the second period. But for the low cost incumbe ...

Chapter 13 Market Structure and Competition Solutions to Review

... 1. Explain why, at a Cournot equilibrium with two firms, neither firm would have any regret about its output choice after it observes the output choice of its rival. In a Cournot setting, each firm chooses a level of output that maximizes its own profit given the output choice of the other firm. In ...

... 1. Explain why, at a Cournot equilibrium with two firms, neither firm would have any regret about its output choice after it observes the output choice of its rival. In a Cournot setting, each firm chooses a level of output that maximizes its own profit given the output choice of the other firm. In ...

1. Definition

... Market –skimming pricing can, in short time, let the enterprise obtain larger profit that then can be used to explore new products. Through this strategy, the marketer sets a relatively high price for a product or service at first leaving a certain leeway. It can also improve product price. This pri ...

... Market –skimming pricing can, in short time, let the enterprise obtain larger profit that then can be used to explore new products. Through this strategy, the marketer sets a relatively high price for a product or service at first leaving a certain leeway. It can also improve product price. This pri ...

chapter overview

... government-granted monopoly privileges. Such rent-seeking may entail substantial costs (lobbying, legal fees, public relations advertising, etc.), which are inefficient. D. Technological progress and dynamic efficiency may occur in some monopolistic industries but not in others. The evidence is mixe ...

... government-granted monopoly privileges. Such rent-seeking may entail substantial costs (lobbying, legal fees, public relations advertising, etc.), which are inefficient. D. Technological progress and dynamic efficiency may occur in some monopolistic industries but not in others. The evidence is mixe ...

Monopoly and Antitrust Policy

... Market Power: Core Concepts • An imperfectly competitive industry is an industry in which single firms have some control over the price of their output. • Market power is the imperfectly competitive firm’s ability to raise price without losing all demand for its product. ...

... Market Power: Core Concepts • An imperfectly competitive industry is an industry in which single firms have some control over the price of their output. • Market power is the imperfectly competitive firm’s ability to raise price without losing all demand for its product. ...

PDF

... the …rst best downstream pricing is equal to the incumbent’s marginal cost. With deregulated downstream (retail) price, La¤ont and Tirole (1994) show that the ECPR holds as a …rst-best pricing rule only when a number of stringent assumptions hold. In particular, ECPR is optimal if the downstream mar ...

... the …rst best downstream pricing is equal to the incumbent’s marginal cost. With deregulated downstream (retail) price, La¤ont and Tirole (1994) show that the ECPR holds as a …rst-best pricing rule only when a number of stringent assumptions hold. In particular, ECPR is optimal if the downstream mar ...

Microeconomics, 4e (Perloff)

... 14) Suppose a consumer advocacy group has convinced legislators that vitamin pills should be free to consumers. Such a policy would enhance the health of the citizenry, they argue. Assuming a downwardsloping linear demand curve and a horizontal long-run supply curve, determine the resulting output a ...

... 14) Suppose a consumer advocacy group has convinced legislators that vitamin pills should be free to consumers. Such a policy would enhance the health of the citizenry, they argue. Assuming a downwardsloping linear demand curve and a horizontal long-run supply curve, determine the resulting output a ...

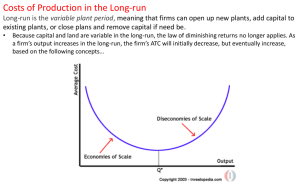

Chapter 10 - Pegasus @ UCF

... decreases as output increases. Diseconomies of Scale exist when LAC increases as output increases. ...

... decreases as output increases. Diseconomies of Scale exist when LAC increases as output increases. ...

Chapter 1

... • A good is called a Giffen good if a decrease in its price causes the quantity demanded to fall. • The Law of Demand was an empirical regularity, not a theoretical necessity. Although it’s theoretically possible for a demand curve to slope upward, economists have found few, if any, real-world examp ...

... • A good is called a Giffen good if a decrease in its price causes the quantity demanded to fall. • The Law of Demand was an empirical regularity, not a theoretical necessity. Although it’s theoretically possible for a demand curve to slope upward, economists have found few, if any, real-world examp ...

Sections 1.0,1.1, pages 297-301.

... - 3 properties of Monopoly: Slide 3 and Section 1.0, pages 249-250. - The 3 barriers to entry: Slides 4-13 and Section 1.1, pages 250-252. - The demand curve for a monopoly firm: Slides 14-15 and Sections 2.0, 2.1, pages 254-255. - Total revenue and price elasticity: Section 2.2 and pages 255-256. - ...

... - 3 properties of Monopoly: Slide 3 and Section 1.0, pages 249-250. - The 3 barriers to entry: Slides 4-13 and Section 1.1, pages 250-252. - The demand curve for a monopoly firm: Slides 14-15 and Sections 2.0, 2.1, pages 254-255. - Total revenue and price elasticity: Section 2.2 and pages 255-256. - ...

File

... A firm with a large share of the total sales in a particular market is a “price-maker”, because to sell more output, it must lower its prices. For this reason… ...

... A firm with a large share of the total sales in a particular market is a “price-maker”, because to sell more output, it must lower its prices. For this reason… ...

Demand, Supply and Pricing

... Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. ...

... Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑