Supply and Demand: An Introduction

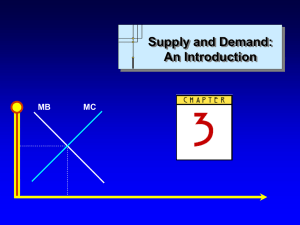

... An Increase In Quantity Supplied vs. An Increase In Supplied Price ...

... An Increase In Quantity Supplied vs. An Increase In Supplied Price ...

(consumer + producer surplus).

... 2. Suppose Gizmo Inc. is willing to sell one gizmo for $10, a second gizmo for $12, a third for $14, and a fourth for $20, and the market price is $20. What is Gizmo Inc.’s producer surplus? a. $56 b. $24 c. $20 d. $10 B. Producer surplus is the difference between the selling price and price produc ...

... 2. Suppose Gizmo Inc. is willing to sell one gizmo for $10, a second gizmo for $12, a third for $14, and a fourth for $20, and the market price is $20. What is Gizmo Inc.’s producer surplus? a. $56 b. $24 c. $20 d. $10 B. Producer surplus is the difference between the selling price and price produc ...

Foundations of Economics, 3e (Bade/Parkin)

... 12) Jason needs help getting ready for the next test in his economics course and would like to hire Maria, an economics tutor to help him. Jason is willing to pay $30 for the first hour of tutoring, $25 for the second, $20 for the third, $15 for the fourth, and $10 for the fifth. The equilibrium pr ...

... 12) Jason needs help getting ready for the next test in his economics course and would like to hire Maria, an economics tutor to help him. Jason is willing to pay $30 for the first hour of tutoring, $25 for the second, $20 for the third, $15 for the fourth, and $10 for the fifth. The equilibrium pr ...

Calculating the Revenue of a Firm

... A shift in the average revenue curve (AR) will also bring about a shift in the marginal revenue curve (MR) Seasonal revenues: Many businesses experience seasonal fluctuations in revenues because the strength of demand ebbs and flow at different times of the year. Good examples of seasonal shifts in ...

... A shift in the average revenue curve (AR) will also bring about a shift in the marginal revenue curve (MR) Seasonal revenues: Many businesses experience seasonal fluctuations in revenues because the strength of demand ebbs and flow at different times of the year. Good examples of seasonal shifts in ...

DOWNLOAD PAPER

... imports completely by setting the home price no higher than the foreign price plus the marginal trade cost. The mere threat of unlimited competition induces price conversion. With (endogenously) limited arbitrage, the manufacturer chooses to accommodate the competition and the home price falls as th ...

... imports completely by setting the home price no higher than the foreign price plus the marginal trade cost. The mere threat of unlimited competition induces price conversion. With (endogenously) limited arbitrage, the manufacturer chooses to accommodate the competition and the home price falls as th ...

Lecture 12, Mergers

... • The preceding example is not a special case; it is easy to show that a merger will almost certainly be unprofitable in the basic Cournot model whether it is between two firms or more than two firms, as long as it does not create a monopoly. • Suppose we have N > 2 firms in a Cournot game. Firms h ...

... • The preceding example is not a special case; it is easy to show that a merger will almost certainly be unprofitable in the basic Cournot model whether it is between two firms or more than two firms, as long as it does not create a monopoly. • Suppose we have N > 2 firms in a Cournot game. Firms h ...

PDF

... Miller, J. E. “Soybeans. ” In Effects of Air Pollution on Farm Commodities. J. S. Jacobson and A. A. MilIens, Eds. (Arlington, VA: Isaak Walton League, ...

... Miller, J. E. “Soybeans. ” In Effects of Air Pollution on Farm Commodities. J. S. Jacobson and A. A. MilIens, Eds. (Arlington, VA: Isaak Walton League, ...

PAGE 1 Econ 2113 - Test 1 Fall 2003 Dr. Rupp Multiple Choice 1

... a. Markets are usually a good way to organize economic activity. b. Markets are usually inferior to central planning as a way to organize economic activity. c. Markets are flawed and are therefore not an acceptable way to organize economic activity. d. Markets are a good way to organize economic act ...

... a. Markets are usually a good way to organize economic activity. b. Markets are usually inferior to central planning as a way to organize economic activity. c. Markets are flawed and are therefore not an acceptable way to organize economic activity. d. Markets are a good way to organize economic act ...

Chapter 4 Demand and Supply

... Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. ...

... Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. ...

1 Efficiency and equity Chapter 5 efficiency and Equity 1 Efficiency

... You could spend the rest of the course talking about and discussing equity, fairness, or distributive justice as it is sometimes called. This material is not standard and you’ll be hard pressed to find it in any other principles text. It is included here because students are very curious about just ...

... You could spend the rest of the course talking about and discussing equity, fairness, or distributive justice as it is sometimes called. This material is not standard and you’ll be hard pressed to find it in any other principles text. It is included here because students are very curious about just ...

PDF

... receives positive surplus from both brands. As a result, each firm maximizes its profit by charging the monopoly price, pm. Here, entry causes consumer surplus to double because the firms do not compete for the same consumers (there are two local monopolies). Now suppose that z < z so that a duopoli ...

... receives positive surplus from both brands. As a result, each firm maximizes its profit by charging the monopoly price, pm. Here, entry causes consumer surplus to double because the firms do not compete for the same consumers (there are two local monopolies). Now suppose that z < z so that a duopoli ...

I`m a teacher - matthewmcgee.com

... the Y-axis and quantity demanded on the X-axis, we would see negative correlation: when the price of a good falls the quantity purchased of the good will increase. The starting point for our model of demand is positing (= proposing) that a rise in the price of a good will lead to lower quantity dema ...

... the Y-axis and quantity demanded on the X-axis, we would see negative correlation: when the price of a good falls the quantity purchased of the good will increase. The starting point for our model of demand is positing (= proposing) that a rise in the price of a good will lead to lower quantity dema ...

Foreign Office warns against travel to Nepal

... flight services that leave Nepal is higher, quantity transacted remains unchanged (Q1) since the supply of flight services is fixed. Since the new air ticket price (P2) is still lower than the equilibrium price, so quantity supplied (Qs) is less than quantity demanded (Qd), and so excess demand ...

... flight services that leave Nepal is higher, quantity transacted remains unchanged (Q1) since the supply of flight services is fixed. Since the new air ticket price (P2) is still lower than the equilibrium price, so quantity supplied (Qs) is less than quantity demanded (Qd), and so excess demand ...

Question 3 - HomeworkForYou

... Given a normal market supply curve for bicycles, if the government required warning labels on all bicycles, then there is a/an ...

... Given a normal market supply curve for bicycles, if the government required warning labels on all bicycles, then there is a/an ...

CHAPTER OVERVIEW

... A. Price, output, and efficiency of resource allocation should be considered. 1. Monopolies will sell a smaller output and charge a higher price than would competitive producers selling in the same market, i.e., assuming similar costs. 2. Monopoly price will exceed marginal cost, because it exceeds ...

... A. Price, output, and efficiency of resource allocation should be considered. 1. Monopolies will sell a smaller output and charge a higher price than would competitive producers selling in the same market, i.e., assuming similar costs. 2. Monopoly price will exceed marginal cost, because it exceeds ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.