Firms in Competitive Markets

... new firms enter, SR market supply shifts right. P falls, reducing profits and slowing entry. If existing firms incur losses, some firms exit, SR market supply shifts left. P rises, reducing remaining firms’ losses. ...

... new firms enter, SR market supply shifts right. P falls, reducing profits and slowing entry. If existing firms incur losses, some firms exit, SR market supply shifts left. P rises, reducing remaining firms’ losses. ...

elasticity notes

... small, either in absolute terms or relative to the change in price. (2) We have discussed that an increase in demand will result in increases in both equilibrium price and quantity. However, we have said nothing about what determines whether the change in either price or quantity is large or small. ...

... small, either in absolute terms or relative to the change in price. (2) We have discussed that an increase in demand will result in increases in both equilibrium price and quantity. However, we have said nothing about what determines whether the change in either price or quantity is large or small. ...

Homework #3

... your name, TA name and section number on top of the homework (legibly). Make sure you write your name as it appears on your ID so that you can receive the correct grade. Please remember the section number for the section you are registered, because you will need that number when you submit exams and ...

... your name, TA name and section number on top of the homework (legibly). Make sure you write your name as it appears on your ID so that you can receive the correct grade. Please remember the section number for the section you are registered, because you will need that number when you submit exams and ...

Slide 1

... When supply is lower than demand then there is a shortage price is the price where and price will increase. When supply is greater than demand supply and demand are then there is a surplus and price should decrease. ...

... When supply is lower than demand then there is a shortage price is the price where and price will increase. When supply is greater than demand supply and demand are then there is a surplus and price should decrease. ...

FRQ Walkthrough #2 Perfectly Competitive Labor Market

... little mini-graph to get it working in my head. If the nominal interest rate increases, then consumers will put their money back into banks to earn interest, and stop spending. Businesses won’t borrow because it costs them more to do so. As such, AD decreases. If AD decreases, APL and real GDP decre ...

... little mini-graph to get it working in my head. If the nominal interest rate increases, then consumers will put their money back into banks to earn interest, and stop spending. Businesses won’t borrow because it costs them more to do so. As such, AD decreases. If AD decreases, APL and real GDP decre ...

Monopolies Lecture - Mr. Tyler`s Lessons

... they would have higher costs. • Having only one electric company keeps prices low Natural Monopoly- It is NATURAL for only one firm to produce because they can produce at the lowest cost. ...

... they would have higher costs. • Having only one electric company keeps prices low Natural Monopoly- It is NATURAL for only one firm to produce because they can produce at the lowest cost. ...

Econ_111-10-13

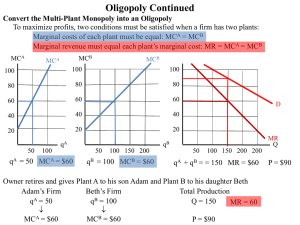

... It is in the collective interests of the firms in an industry to establish a cartel to maximize their joint profits by reducing production below the competitive level. But, if a cartel is established it may be in the individual interests of each firm to cheat on the cartel agreement by producing mor ...

... It is in the collective interests of the firms in an industry to establish a cartel to maximize their joint profits by reducing production below the competitive level. But, if a cartel is established it may be in the individual interests of each firm to cheat on the cartel agreement by producing mor ...

FREE Sample Here

... Labour cost measures the same equation in dollars. The dollar value of outputs is divided by the dollar value of the work hours to arrive at the labour cost per unit. Anything that increases productivity or reduces labour costs makes a business, and country, more competitive because prices can be lo ...

... Labour cost measures the same equation in dollars. The dollar value of outputs is divided by the dollar value of the work hours to arrive at the labour cost per unit. Anything that increases productivity or reduces labour costs makes a business, and country, more competitive because prices can be lo ...

A professor hires two aides, assigning them the tasks of reading

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

Macroeconomics Topic 8: “Explain how slow price

... assume that sellers do not know all prices at all times, then an unexpected drop in the price level may cause some sellers to mistakenly believe that the relative price of the product they sell has declined. This will lead them to reduce output. For example, suppose ALL prices fall by 10%, so that n ...

... assume that sellers do not know all prices at all times, then an unexpected drop in the price level may cause some sellers to mistakenly believe that the relative price of the product they sell has declined. This will lead them to reduce output. For example, suppose ALL prices fall by 10%, so that n ...

Imperfect Competition

... Model Assumptions: Monopolistic Competition 1. Industry firms sell differentiated products that consumers do not view as perfect ...

... Model Assumptions: Monopolistic Competition 1. Industry firms sell differentiated products that consumers do not view as perfect ...

Marketing - cungeheier

... available resources are among the factors in production that must be considered by both private and governmental producers.” ...

... available resources are among the factors in production that must be considered by both private and governmental producers.” ...

Document

... 2. If consumers are relatively unresponsive to price changes, demand is said to be inelastic. 3. Note that with both elastic and inelastic demand, consumers behave according to the law of demand; that is, they are responsive to price changes. The terms elastic or inelastic describe the degree of res ...

... 2. If consumers are relatively unresponsive to price changes, demand is said to be inelastic. 3. Note that with both elastic and inelastic demand, consumers behave according to the law of demand; that is, they are responsive to price changes. The terms elastic or inelastic describe the degree of res ...

File

... good that consumers demand more of when their incomes increase. An inferior good is a good that consumers demand less of when their income increases. Chapter 4 ...

... good that consumers demand more of when their incomes increase. An inferior good is a good that consumers demand less of when their income increases. Chapter 4 ...

Lecture 5: March 30 5.1 Introduction 5.2 Proof of existence of

... player plays V and C with a positive probability it follows that the joint utility is below 2. By the linearity of expectation it follows that at least one player has utility below 1. This player is better off playing purely f and thus V or C are never played in a Nash Equilibrium. 3. Thus we can as ...

... player plays V and C with a positive probability it follows that the joint utility is below 2. By the linearity of expectation it follows that at least one player has utility below 1. This player is better off playing purely f and thus V or C are never played in a Nash Equilibrium. 3. Thus we can as ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.