research paper series Research Paper 2007/33

... productive and less volatile firms are replaced with highly productive and volatile ones. However, in the second case, trade does not necessarily raise average productivity in the market. Our analysis also shows that more volatile firms generally have more incentives to trade than their less volatil ...

... productive and less volatile firms are replaced with highly productive and volatile ones. However, in the second case, trade does not necessarily raise average productivity in the market. Our analysis also shows that more volatile firms generally have more incentives to trade than their less volatil ...

News Release

... The estimated Solvency II ratio represents the shareholder view. This ratio excludes the contribution to Group Solvency Capital Requirement (‘SCR’) and Group Own Funds of fully ring-fenced with-profits funds (£2.7 billion) and staff pension schemes in surplus (£0.7 billion) – these exclusions have n ...

... The estimated Solvency II ratio represents the shareholder view. This ratio excludes the contribution to Group Solvency Capital Requirement (‘SCR’) and Group Own Funds of fully ring-fenced with-profits funds (£2.7 billion) and staff pension schemes in surplus (£0.7 billion) – these exclusions have n ...

Tier 1 capital

... General Reserve for Credit Losses ............................................................ 37 Hybrid capital instruments .......................................................................... 37 Lower Tier 2 capital ............................................................................ ...

... General Reserve for Credit Losses ............................................................ 37 Hybrid capital instruments .......................................................................... 37 Lower Tier 2 capital ............................................................................ ...

Negotiating an Equity Capital Infusion from Outside Investors

... from outside investors. To facilitate this understanding, this guide includes a sample annotated equity offering Term Sheet (the document that is often used by an MFI in the early stages of an equity infusion negotiation) as well as a Shareholders Agreement and an annotated Share Subscription Agreem ...

... from outside investors. To facilitate this understanding, this guide includes a sample annotated equity offering Term Sheet (the document that is often used by an MFI in the early stages of an equity infusion negotiation) as well as a Shareholders Agreement and an annotated Share Subscription Agreem ...

the effect of product market competition on

... factories it contracts with overseas. As a result, these and other companies have passed their own internal code of conduct to establish labor guidelines not only for their own employees but also for their suppliers. Other consumer boycotts over social or environmental issues have forced companies t ...

... factories it contracts with overseas. As a result, these and other companies have passed their own internal code of conduct to establish labor guidelines not only for their own employees but also for their suppliers. Other consumer boycotts over social or environmental issues have forced companies t ...

ASX Clear Schedule 01 - Risk Based Capital Requirements

... Exchange Derivative by ASX Clear. “Debt Equivalent” means the value of a position in a Debt Derivative that is equivalent to the value had it been a physical position in the underlying Debt Instrument calculated in accordance with clause 16 of Annexure 3. ...

... Exchange Derivative by ASX Clear. “Debt Equivalent” means the value of a position in a Debt Derivative that is equivalent to the value had it been a physical position in the underlying Debt Instrument calculated in accordance with clause 16 of Annexure 3. ...

Reforms to the UK takeover regime – a guide

... intentions of a potential competing offeror (that has been named or whose existence has been disclosed by the offeree) during the later stages of an existing firm offer (the so-called “Day 50 rule”) is now codified. This will apply even if the potential offeror was subject to a no intention to bid s ...

... intentions of a potential competing offeror (that has been named or whose existence has been disclosed by the offeree) during the later stages of an existing firm offer (the so-called “Day 50 rule”) is now codified. This will apply even if the potential offeror was subject to a no intention to bid s ...

Customer Equity Evaluation: A Study With Reference to Jammu and

... performing with regard to the tactical decisions it makes in handling and extracting value from the customer. Academic researchers have written scores of articles and books on this topic (for examples; Rust, Zeithaml & Lemon, 2000; Blattberg, Getz & Thomas, 2001; Gupta & Lehmann, 2005). The growing ...

... performing with regard to the tactical decisions it makes in handling and extracting value from the customer. Academic researchers have written scores of articles and books on this topic (for examples; Rust, Zeithaml & Lemon, 2000; Blattberg, Getz & Thomas, 2001; Gupta & Lehmann, 2005). The growing ...

Uncertainty in Executive Compensation and Capital Investment: A Panel Study

... last years in office and argue that this is puzzling since incentive compensation plans typically are not tied to shareholder value. Rather, the compensation package usually depends on accounting performance which the CEOs should want to keep high in their final years in office. None of these papers ...

... last years in office and argue that this is puzzling since incentive compensation plans typically are not tied to shareholder value. Rather, the compensation package usually depends on accounting performance which the CEOs should want to keep high in their final years in office. None of these papers ...

25.03.2013 rule 2.7 announcement

... “Cazenove Capital’s culture of client focus and investment excellence are a strong fit with Schroders. This transaction creates a leading, independent Private Banking and Wealth Management business in the UK, and brings additional investment talent in complementary strategies across UK and European ...

... “Cazenove Capital’s culture of client focus and investment excellence are a strong fit with Schroders. This transaction creates a leading, independent Private Banking and Wealth Management business in the UK, and brings additional investment talent in complementary strategies across UK and European ...

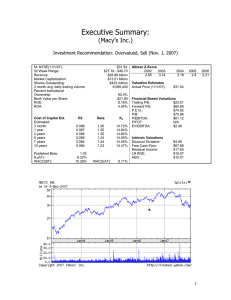

Macy's Inc. - Mark E. Moore

... has been growing steadily over the last five years, and Macy’s sales were low until 2005 when their sales shot up. Therefore, just because the industry in general shows slow growth a firm can be innovative and still show growth. Most firms grow by acquiring new stores or diversifying into other area ...

... has been growing steadily over the last five years, and Macy’s sales were low until 2005 when their sales shot up. Therefore, just because the industry in general shows slow growth a firm can be innovative and still show growth. Most firms grow by acquiring new stores or diversifying into other area ...

Expected Returns on Major Asset Classes

... we chose Dr. Ilmanen’s chapters on that topic as the basis for this book. Readers interested in application of his methods to more exotic fields should consult Expected Returns (2011a), which we heartily endorse, not only because its writing was supported by the Research Foundation of CFA Institute ...

... we chose Dr. Ilmanen’s chapters on that topic as the basis for this book. Readers interested in application of his methods to more exotic fields should consult Expected Returns (2011a), which we heartily endorse, not only because its writing was supported by the Research Foundation of CFA Institute ...

Pride and Prestige: Why Some Firms Pay Their CEOs Less

... top 100 of the FTMA list earn on average 9% less compared to CEOs of companies that are not admired after controlling for a range of other factors. These results are obtained based on panel regressions with a large range of controls and fixed effects; they also hold if we include firm fixed effects. ...

... top 100 of the FTMA list earn on average 9% less compared to CEOs of companies that are not admired after controlling for a range of other factors. These results are obtained based on panel regressions with a large range of controls and fixed effects; they also hold if we include firm fixed effects. ...

Global perspectives: 2016 REIT report

... capital; rather, owners took advantage of the SOCIMI structure as a more favorable tax wrapper in which to hold existing assets. In 2014, four SOCIMIs listed on the Continuo (main) market, raising US$3.6b of equity capital.6 This group has seen its market cap grow 72% to US$6.2b7 today. Transaction ...

... capital; rather, owners took advantage of the SOCIMI structure as a more favorable tax wrapper in which to hold existing assets. In 2014, four SOCIMIs listed on the Continuo (main) market, raising US$3.6b of equity capital.6 This group has seen its market cap grow 72% to US$6.2b7 today. Transaction ...

Fair Value Measurements and Disclosures (Topic 820)

... values as defined in the Master Glossary of the FASB Accounting Standards Codification™ (because, for example, those investments are not listed on national exchanges or over-the-counter markets such as the National Association of Securities Dealers Automated Quotation System). Examples of these inve ...

... values as defined in the Master Glossary of the FASB Accounting Standards Codification™ (because, for example, those investments are not listed on national exchanges or over-the-counter markets such as the National Association of Securities Dealers Automated Quotation System). Examples of these inve ...

Is Business Saving Really None of Our Business

... implying that three-quarters of total assets are paid for with equity, most of it internally generated. For six big Latin American countries in 2009, Bebczuk and Galindo (2010) also find this ratio to be 26 percent. For developed economies, the number is even lower (20 percent), suggesting that heav ...

... implying that three-quarters of total assets are paid for with equity, most of it internally generated. For six big Latin American countries in 2009, Bebczuk and Galindo (2010) also find this ratio to be 26 percent. For developed economies, the number is even lower (20 percent), suggesting that heav ...

Dividend Policy, Strategy and Analysis

... would the shares trade? Fortunately companies that can pay dividends eventually do. According to MM, a company’s dividend policy is irrelevant even for shareholders who want a present cash return. If the company does not pay dividends, investors are free to do what the shareholders of any “frozen co ...

... would the shares trade? Fortunately companies that can pay dividends eventually do. According to MM, a company’s dividend policy is irrelevant even for shareholders who want a present cash return. If the company does not pay dividends, investors are free to do what the shareholders of any “frozen co ...

Expected Returns on Major Asset Classes

... we chose Dr. Ilmanen’s chapters on that topic as the basis for this book. Readers interested in application of his methods to more exotic fields should consult Expected Returns (2011a), which we heartily endorse, not only because its writing was supported by the Research Foundation of CFA Institute ...

... we chose Dr. Ilmanen’s chapters on that topic as the basis for this book. Readers interested in application of his methods to more exotic fields should consult Expected Returns (2011a), which we heartily endorse, not only because its writing was supported by the Research Foundation of CFA Institute ...

Debt Maturity and the Dynamics of Leverage

... asymmetries or agency conflicts. In the model firms’ equityholders are allowed to optimize the mix of debt and equity used to refinance maturing debt, but covenants do not allow them to increase the total face value of debt. If firms wish to do increase the face value of debt they must first repurch ...

... asymmetries or agency conflicts. In the model firms’ equityholders are allowed to optimize the mix of debt and equity used to refinance maturing debt, but covenants do not allow them to increase the total face value of debt. If firms wish to do increase the face value of debt they must first repurch ...

Report submitted by Alternative Investment Policy Advisory

... 4. Alternative Investment Funds, include venture capital and private equity funds, which provide stable, long-term capital and have fund lives ranging typically up to 10 years or more. AIFs include funds with a wide range of investment objectives and investment strategies. These include investing in ...

... 4. Alternative Investment Funds, include venture capital and private equity funds, which provide stable, long-term capital and have fund lives ranging typically up to 10 years or more. AIFs include funds with a wide range of investment objectives and investment strategies. These include investing in ...

Capital Flows to Central and Eastern Europe and the Former Soviet

... low level of private inflows was due to a variety of factors, including partial and incomplete reforms or an uncertain commitment to reform in most countries, high political and social costs of the transition process itself, and high levels of corruption and political instability (several countries ...

... low level of private inflows was due to a variety of factors, including partial and incomplete reforms or an uncertain commitment to reform in most countries, high political and social costs of the transition process itself, and high levels of corruption and political instability (several countries ...

Heterogeneous exits: Evidence from new firms

... ignoring heterogeneity between forms of exit would yield incorrect interpretations. To provide a better understanding of industry dynamics, including entry and exit, we explore heterogeneous exits—bankruptcy, voluntary liquidation, and merger—by focusing on new firms. In particular, we examine empir ...

... ignoring heterogeneity between forms of exit would yield incorrect interpretations. To provide a better understanding of industry dynamics, including entry and exit, we explore heterogeneous exits—bankruptcy, voluntary liquidation, and merger—by focusing on new firms. In particular, we examine empir ...

Market Reaction to the Adoption of IFRS in Europe Working Paper

... To assess whether investors reacted differently to IFRS adoption events as a function of firms’ information asymmetry and accounting standards enforcement, as well as their preadoption information quality, we estimate the cross-sectional relation between firms’ event returns and proxies for these c ...

... To assess whether investors reacted differently to IFRS adoption events as a function of firms’ information asymmetry and accounting standards enforcement, as well as their preadoption information quality, we estimate the cross-sectional relation between firms’ event returns and proxies for these c ...

Corporate Governance And Earnings

... activities with good business practices, objectivity, and integrity. Sound corporate governance is reliant on external marketplace commitment and legislation, as well as a healthy board culture that safeguards policies and processes. Corporate governance is designed to pursue stakeholders’ interests ...

... activities with good business practices, objectivity, and integrity. Sound corporate governance is reliant on external marketplace commitment and legislation, as well as a healthy board culture that safeguards policies and processes. Corporate governance is designed to pursue stakeholders’ interests ...

Private equity in the 1980s

Private equity in the 1980s relates to one of the major periods in the history of private equity and venture capital. Within the broader private equity industry, two distinct sub-industries, leveraged buyouts and venture capital experienced growth along parallel although interrelated tracks.The development of the private equity and venture capital asset classes has occurred through a series of boom and bust cycles since the middle of the 20th century. The 1980s saw the first major boom and bust cycle in private equity. The cycle which is typically marked by the 1982 acquisition of Gibson Greetings and ending just over a decade later was characterized by a dramatic surge in leveraged buyout (LBO) activity financed by junk bonds. The period culminated in the massive buyout of RJR Nabisco before the near collapse of the leveraged buyout industry in the late 1980s and early 1990s marked by the collapse of Drexel Burnham Lambert and the high-yield debt market.