International Financial Integration and Crisis Contagion ∗ Michael B. Devereux Changhua Yu

... While we find that financial crises are more likely in an integrated world financial market, crises are much less severe in terms of lost output and consumption than those in financial autarky. During ‘normal times’ (or in the absence of crises), the impact of financial integration is rather small ...

... While we find that financial crises are more likely in an integrated world financial market, crises are much less severe in terms of lost output and consumption than those in financial autarky. During ‘normal times’ (or in the absence of crises), the impact of financial integration is rather small ...

The Role of Private Investment in Meeting U.S. Transportation

... ARTBA believed it was an ideal time to take an objective look at where the P3 market stands today after almost two decades of active promotion and assistance at the federal level. This is particularly important as leaders from both political parties increasingly suggest that private investment must ...

... ARTBA believed it was an ideal time to take an objective look at where the P3 market stands today after almost two decades of active promotion and assistance at the federal level. This is particularly important as leaders from both political parties increasingly suggest that private investment must ...

On the Cross-Section of Expected Returns of German Stocks: A Re

... information about small and large firms and thus related to the perceived riskiness of small firm stocks.9 This hypothesis was also tested by Amihud and Mendelson (1989), who proxy the information factor of an asset by its bid-ask spread. Their results suggest that only systematic risk and a stock’s ...

... information about small and large firms and thus related to the perceived riskiness of small firm stocks.9 This hypothesis was also tested by Amihud and Mendelson (1989), who proxy the information factor of an asset by its bid-ask spread. Their results suggest that only systematic risk and a stock’s ...

Download attachment

... stocks, in general, are permitted from the religious perspective, the MCos., do not offer to their investors, much different investment opportunities compared to common stocks. Second, unlike deposit mobilization by the Islamic banks, the resource mobilization requirements of the MCos., compel them ...

... stocks, in general, are permitted from the religious perspective, the MCos., do not offer to their investors, much different investment opportunities compared to common stocks. Second, unlike deposit mobilization by the Islamic banks, the resource mobilization requirements of the MCos., compel them ...

The IPO Exit

... Companies controlled by a sponsor following an IPO need to consider whether to include provisions in their organizational documents that enable them to retain control over such companies. Common provisions include multiple or dual-class share classes with disparate voting rights and veto rights, or ...

... Companies controlled by a sponsor following an IPO need to consider whether to include provisions in their organizational documents that enable them to retain control over such companies. Common provisions include multiple or dual-class share classes with disparate voting rights and veto rights, or ...

Vertical monopoly power, profit and risk: The British beer industry, c

... at key stages in the value chain. In the absence of integration, powerful operators can exercise dominance through direct contract specification motivated by cost minimisation.10 A specific aspect of the brewery tie and Pubco models that has not hitherto been investigated is the question of how much ...

... at key stages in the value chain. In the absence of integration, powerful operators can exercise dominance through direct contract specification motivated by cost minimisation.10 A specific aspect of the brewery tie and Pubco models that has not hitherto been investigated is the question of how much ...

QUESTIONS

... company were sold to another company. 16. The book value per share calculation of a corporation is usually significantly different from the market value of the stock’s selling price due to the A. Use of accrual accounting in preparing financial statements. B. Omission of the number of preferred shar ...

... company were sold to another company. 16. The book value per share calculation of a corporation is usually significantly different from the market value of the stock’s selling price due to the A. Use of accrual accounting in preparing financial statements. B. Omission of the number of preferred shar ...

The Institutional Construction of Firms

... governance of firms needs to consider how dominant interest groups and institutions influence the construction, direction and development of major companies in different jurisdictions in such ways that their behaviour and economic consequences vary. While this clearly involves issues of ownership an ...

... governance of firms needs to consider how dominant interest groups and institutions influence the construction, direction and development of major companies in different jurisdictions in such ways that their behaviour and economic consequences vary. While this clearly involves issues of ownership an ...

Unlocking funding for European investment and growth

... Europe is not alone in experiencing sluggish growth, but what is notable is that since 2008, both the real economy and the financial sector in Europe have suffered continued setbacks. This report focuses on the role of finance in supporting growth. It examines the obstacles which currently prevent t ...

... Europe is not alone in experiencing sluggish growth, but what is notable is that since 2008, both the real economy and the financial sector in Europe have suffered continued setbacks. This report focuses on the role of finance in supporting growth. It examines the obstacles which currently prevent t ...

Do Private Firms Perform Better than Public Firms?

... We note the earlier contribution by Ke, Petroni, and Safieddine (1999), who use a very small sample of public and private insurance companies to show that operating profitability of public and private firms are not significantly different from each other. 4 Bharath and Ditmar (2010) argue that finan ...

... We note the earlier contribution by Ke, Petroni, and Safieddine (1999), who use a very small sample of public and private insurance companies to show that operating profitability of public and private firms are not significantly different from each other. 4 Bharath and Ditmar (2010) argue that finan ...

Do Institutional Investors Alleviate Agency Problems

... issues are greater than stock repurchases, the repurchase amount is set to zero. Changes in repurchases are measured as the repurchases of the current year minus repurchases of the previous year, divided by the book value of assets from the previous year. Changes in dividends are measured similarly. ...

... issues are greater than stock repurchases, the repurchase amount is set to zero. Changes in repurchases are measured as the repurchases of the current year minus repurchases of the previous year, divided by the book value of assets from the previous year. Changes in dividends are measured similarly. ...

Do Banks Really Care? Social Norms in Bank Lending This version

... valuation losses relative to non-sin firms. Similarly, countries where these industries are not shunned by societal views do not experience valuation differences with otherwise similar firms. The authors conclude that there is a significant relation between social views and equity market valuation ...

... valuation losses relative to non-sin firms. Similarly, countries where these industries are not shunned by societal views do not experience valuation differences with otherwise similar firms. The authors conclude that there is a significant relation between social views and equity market valuation ...

pozen inc. - corporate

... Tribute, no par value per share (“ Tribute Shares ”), at a price per share, subject to certain adjustments, equal to (a) the lesser of (i) $7.20, and (ii) a 5% discount off the five day volume weighted average price as reported on Bloomberg Financial Markets per share of Pozen common stock, $0.001 p ...

... Tribute, no par value per share (“ Tribute Shares ”), at a price per share, subject to certain adjustments, equal to (a) the lesser of (i) $7.20, and (ii) a 5% discount off the five day volume weighted average price as reported on Bloomberg Financial Markets per share of Pozen common stock, $0.001 p ...

Determinants of Capital Structure: Evidence from a Major

... been extensive theoretical work on the determinants of firms’ capital structures. Already by the early 1980s, these efforts culminated in the development of the two major theories of capital structure. In the (static) trade-off theory, firms trade off tax savings from debt financing against deadweig ...

... been extensive theoretical work on the determinants of firms’ capital structures. Already by the early 1980s, these efforts culminated in the development of the two major theories of capital structure. In the (static) trade-off theory, firms trade off tax savings from debt financing against deadweig ...

Debt/Equity Swaps and Mexican Law: The

... to stimulate import substitution. 8 In the early 1970s, the only legal restraints on the percentage of foreign participation in industrialized activities resulted from the application of the Emergency Decree of 1944 and the exclusion of private participation, both domestic and foreign, in nationaliz ...

... to stimulate import substitution. 8 In the early 1970s, the only legal restraints on the percentage of foreign participation in industrialized activities resulted from the application of the Emergency Decree of 1944 and the exclusion of private participation, both domestic and foreign, in nationaliz ...

The Leverage Rotation Strategy

... and return. Low volatility stocks have exhibited above market performance with lower than market Beta, challenging the risk/return laws of the CAPM.2 Similarly perplexing is the tendency for high beta stocks to exhibit lower performance than predicted by their level of risk.3 In this paper, we propo ...

... and return. Low volatility stocks have exhibited above market performance with lower than market Beta, challenging the risk/return laws of the CAPM.2 Similarly perplexing is the tendency for high beta stocks to exhibit lower performance than predicted by their level of risk.3 In this paper, we propo ...

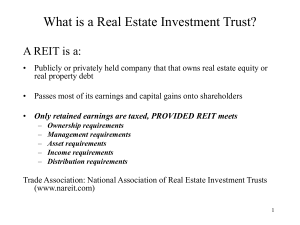

Real Estate Investment Trusts (REITs)

... corporation, TCO, owns units in the TRG real estate partnership. It is this partnership that actually houses the UPREIT's assets, primarily shopping malls. Investors can purchase common stock in the corporation, while investors with direct ownership in the real estate partnership hold preferred shar ...

... corporation, TCO, owns units in the TRG real estate partnership. It is this partnership that actually houses the UPREIT's assets, primarily shopping malls. Investors can purchase common stock in the corporation, while investors with direct ownership in the real estate partnership hold preferred shar ...

ca-ipcc (1st group) financial management (71 imp questions)

... (i) This method of evaluating proposals for capital budgeting is quite simple and easy to understand. It has the advantage of making it clear that there is no profit on any project unless the payback period is over. Further, when funds are limited, they may be made to do more by selecting projects h ...

... (i) This method of evaluating proposals for capital budgeting is quite simple and easy to understand. It has the advantage of making it clear that there is no profit on any project unless the payback period is over. Further, when funds are limited, they may be made to do more by selecting projects h ...

The market has seen leveraged and inverse exchange

... ETFs and use the products, including L&I ETFs, for short-term trading purposes. Asset owners in Taiwan have increasingly used L&I ETFs for speculation, arbitrage and hedging “That demand has driven the rapid growth of L&I ETFs in Taiwan in the past two years,” Julian Liu, president and chief executi ...

... ETFs and use the products, including L&I ETFs, for short-term trading purposes. Asset owners in Taiwan have increasingly used L&I ETFs for speculation, arbitrage and hedging “That demand has driven the rapid growth of L&I ETFs in Taiwan in the past two years,” Julian Liu, president and chief executi ...

Chapter 11 Dividend Policy

... 1.2.1 Retained earnings is surplus cash that has not been needed for operating costs, interest payments, tax liabilities, asset replacement or cash dividends. For many businesses, the cash needed to finance investments will be available because the earnings the business has made have been retained w ...

... 1.2.1 Retained earnings is surplus cash that has not been needed for operating costs, interest payments, tax liabilities, asset replacement or cash dividends. For many businesses, the cash needed to finance investments will be available because the earnings the business has made have been retained w ...

PDF

... Decay is the loss of productive capacity that affects each individual machine while in use. A one year old tractor will require less repair and perform better than the same tractor 5 years later. In special cases („one-hoss-shay“) is possible to imagine that there is no decay, say for a light bulb t ...

... Decay is the loss of productive capacity that affects each individual machine while in use. A one year old tractor will require less repair and perform better than the same tractor 5 years later. In special cases („one-hoss-shay“) is possible to imagine that there is no decay, say for a light bulb t ...

Why Would Chinese Firms List Overseas? (PDF Available)

... enterprises (SOEs) in an overseas market instead of the domestic market, by examining a group of Chinese SOEs with SIPs in Hong Kong. 1 Such an investigation is interesting and important as the phenomenon seems to be inconsistent with existing lines of literature. First, in the cross-listing literat ...

... enterprises (SOEs) in an overseas market instead of the domestic market, by examining a group of Chinese SOEs with SIPs in Hong Kong. 1 Such an investigation is interesting and important as the phenomenon seems to be inconsistent with existing lines of literature. First, in the cross-listing literat ...

Impacting Cancer

... * IND: Investigational New Drug: regulatory application necessary for human trials; NDA/BLA: New Drug Application/Biologics License Application: Regulatory application necessary ...

... * IND: Investigational New Drug: regulatory application necessary for human trials; NDA/BLA: New Drug Application/Biologics License Application: Regulatory application necessary ...

Does direct foreign investment affect domestic firms

... higher correlations between either investment and cash flow (FHP), or between investment and debt to asset ratios and interest coverage (Whited (1992)). Kaplan and Zingales (1997) have criticized this approach, arguing that firms which are identified as credit constrained by FHP are in fact not cons ...

... higher correlations between either investment and cash flow (FHP), or between investment and debt to asset ratios and interest coverage (Whited (1992)). Kaplan and Zingales (1997) have criticized this approach, arguing that firms which are identified as credit constrained by FHP are in fact not cons ...

IOSR Journal of Humanities and Social Science (JHSS)

... perceptible slide in the ratio of private sector investment to GDP despite the emphasis on private sector following the initiation of public sector reform is worrisome. In the light of this background, our researcher findings are quite different from the earlier studies. This is because three of the ...

... perceptible slide in the ratio of private sector investment to GDP despite the emphasis on private sector following the initiation of public sector reform is worrisome. In the light of this background, our researcher findings are quite different from the earlier studies. This is because three of the ...

Private equity in the 1980s

Private equity in the 1980s relates to one of the major periods in the history of private equity and venture capital. Within the broader private equity industry, two distinct sub-industries, leveraged buyouts and venture capital experienced growth along parallel although interrelated tracks.The development of the private equity and venture capital asset classes has occurred through a series of boom and bust cycles since the middle of the 20th century. The 1980s saw the first major boom and bust cycle in private equity. The cycle which is typically marked by the 1982 acquisition of Gibson Greetings and ending just over a decade later was characterized by a dramatic surge in leveraged buyout (LBO) activity financed by junk bonds. The period culminated in the massive buyout of RJR Nabisco before the near collapse of the leveraged buyout industry in the late 1980s and early 1990s marked by the collapse of Drexel Burnham Lambert and the high-yield debt market.