4Q 2015 FR Y-9C Transmittal Letter

... the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the acquirer reports provisional amounts in its financial statements for the items for which the accounting is incomplete. During the measurement period, the acquirer i ...

... the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the acquirer reports provisional amounts in its financial statements for the items for which the accounting is incomplete. During the measurement period, the acquirer i ...

The Sukuk Market Comes of Age - Franklin Templeton Hong Kong

... secular legislation under which they were issued, just like conventional bonds. How Are Sukuk Structured? Although there are various kinds of Sukuk structures, depending on the nature of the underlying asset (see below), they all endeavor to generate returns for investors without infringing on Shari ...

... secular legislation under which they were issued, just like conventional bonds. How Are Sukuk Structured? Although there are various kinds of Sukuk structures, depending on the nature of the underlying asset (see below), they all endeavor to generate returns for investors without infringing on Shari ...

Old Globe Theatre dba The Old Globe

... The Old Globe is the beneficiary of an irrevocable charitable remainder trust administered by a third party. The trust terminates upon the death of the grantor, at which time The Old Globe will receive the remaining trust assets. The fair value of the future benefits to b ...

... The Old Globe is the beneficiary of an irrevocable charitable remainder trust administered by a third party. The trust terminates upon the death of the grantor, at which time The Old Globe will receive the remaining trust assets. The fair value of the future benefits to b ...

venture capital pre-investment decision making process

... enture capitalists (VCs) are professionals who pool funds from high net worth investors and invests these funds into promising young business enterprises (Jain, 1999). Traditionally, companies that have yet to meet listing requirements or qualify for bank loans (Florin, 2005) recognize VC as provide ...

... enture capitalists (VCs) are professionals who pool funds from high net worth investors and invests these funds into promising young business enterprises (Jain, 1999). Traditionally, companies that have yet to meet listing requirements or qualify for bank loans (Florin, 2005) recognize VC as provide ...

Regulation of CrowdFunding in Germany, the UK, Spain and Italy

... are using bank loans while some 40% rely on short-term bank credit or overdraft facilities. On the investment side, venture capital, according to industry statistics, invests in less than 5,000 high-growth businesses a year and business angels in around 1,000. Of the millions of SMEs that are not ac ...

... are using bank loans while some 40% rely on short-term bank credit or overdraft facilities. On the investment side, venture capital, according to industry statistics, invests in less than 5,000 high-growth businesses a year and business angels in around 1,000. Of the millions of SMEs that are not ac ...

Emerging Equity Markets in a Globalizing World

... “Portfolio Flows to Emerging Markets”. At the time, the World Bank had recently compiled the first-ever database of emerging market equity returns. Foreign portfolio (as opposed to direct) investment was relatively new. The theme of the conference was to better understand the risks that portfolio in ...

... “Portfolio Flows to Emerging Markets”. At the time, the World Bank had recently compiled the first-ever database of emerging market equity returns. Foreign portfolio (as opposed to direct) investment was relatively new. The theme of the conference was to better understand the risks that portfolio in ...

NBER WORKING PAPER SERIES M. Ayhan Kose

... and possibly adverse effects of capital account liberalization.4 Shifts in the direction of capital flows can induce or exacerbate boom-bust cycles in developing countries that lack deep financial sectors (Aghion and Banerjee, 2005). Moreover, mismanaged domestic financial sector liberalizations hav ...

... and possibly adverse effects of capital account liberalization.4 Shifts in the direction of capital flows can induce or exacerbate boom-bust cycles in developing countries that lack deep financial sectors (Aghion and Banerjee, 2005). Moreover, mismanaged domestic financial sector liberalizations hav ...

A theory of corporate spin-offs

... returns for parent firms on the announcement date, both spin-offs and their parents experience significantly positive abnormal returns for up to three years beyond the spin-offs’ announcement date. Further, both spin-offs and their parents experience significantly more takeovers than do control groups ...

... returns for parent firms on the announcement date, both spin-offs and their parents experience significantly positive abnormal returns for up to three years beyond the spin-offs’ announcement date. Further, both spin-offs and their parents experience significantly more takeovers than do control groups ...

FAQs by Issuers

... economy, industry, capital markets and companies. We also conduct training programs to financial sector professionals on a wide array of technical issues. We are India's most credible provider of economy and industry research. Our industry research covers 86 sectors and is known for its rich insight ...

... economy, industry, capital markets and companies. We also conduct training programs to financial sector professionals on a wide array of technical issues. We are India's most credible provider of economy and industry research. Our industry research covers 86 sectors and is known for its rich insight ...

When does corporate venture capital investment

... investment vehicle. CVC investors often suffer from rampant information asymmetries. Entrepreneurial ventures have private information about their future prospects that are often not directly observable by potential investors (Gans and Stern, 2003). This may lead to adverse selection as low-quality ...

... investment vehicle. CVC investors often suffer from rampant information asymmetries. Entrepreneurial ventures have private information about their future prospects that are often not directly observable by potential investors (Gans and Stern, 2003). This may lead to adverse selection as low-quality ...

- Columbia Business School

... exist skilled fund managers who have more accurate information, and they will use their current information about the market to identify who are actually skilled. The outperformance of the funds with MT-sensitive inflows when compared to various alternative investments supports this idea. This is re ...

... exist skilled fund managers who have more accurate information, and they will use their current information about the market to identify who are actually skilled. The outperformance of the funds with MT-sensitive inflows when compared to various alternative investments supports this idea. This is re ...

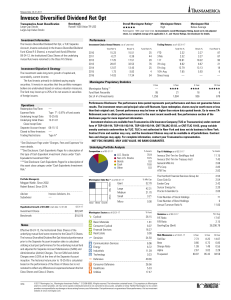

Invesco Diversified Dividend Ret Opt

... Performance Disclosure: The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value will fluctuate. Upon redemption, shares may be worth more or less than their original cost. Current performance may be lower or higher than ...

... Performance Disclosure: The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value will fluctuate. Upon redemption, shares may be worth more or less than their original cost. Current performance may be lower or higher than ...

Why do we invest ethically?

... segmentation, contrary to mainstream expectations at the time, did exist to the extent that individual preferences could hinder the free flow of capital and interfere with the establishment of coherent risk-return relationships among securities. They isolated five different investor groups with diff ...

... segmentation, contrary to mainstream expectations at the time, did exist to the extent that individual preferences could hinder the free flow of capital and interfere with the establishment of coherent risk-return relationships among securities. They isolated five different investor groups with diff ...

SunAmerica Dynamic Allocation Portfolio Summary

... 80% of its assets to Underlying Portfolios investing primarily in equity securities and 20% to 50% of its assets to Underlying Portfolios investing primarily in fixed income securities and short-term investments, which may include mortgage- and asset-backed securities, to seek capital appreciation a ...

... 80% of its assets to Underlying Portfolios investing primarily in equity securities and 20% to 50% of its assets to Underlying Portfolios investing primarily in fixed income securities and short-term investments, which may include mortgage- and asset-backed securities, to seek capital appreciation a ...

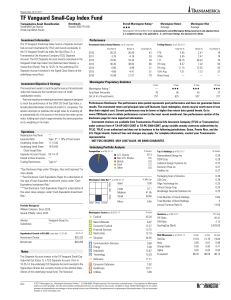

TF Vanguard Small-Cap Index Fund

... Performance Disclosure: The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value will fluctuate. Upon redemption, shares may be worth more or less than their original cost. Current performance may be lower or higher than ...

... Performance Disclosure: The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value will fluctuate. Upon redemption, shares may be worth more or less than their original cost. Current performance may be lower or higher than ...

Community Investment

... which aim to provide an affordable service, such as social housing or low-cost office space for community projects. Instead of the society having to make and retain profits to provide the reserves it needs to acquire assets, the enterprise can rent the capital it needs from members. Withdrawable sha ...

... which aim to provide an affordable service, such as social housing or low-cost office space for community projects. Instead of the society having to make and retain profits to provide the reserves it needs to acquire assets, the enterprise can rent the capital it needs from members. Withdrawable sha ...

UNCTAD`s Global Action Menu for Investment Facilitation

... Overall, the number of investment facilitation measures adopted by countries over the past six years remains relatively low compared with the numbers of other investment promotion measures. In addition, only about 20 per cent of the 111 investment laws analyzed by UNCTAD deal with specific aspects o ...

... Overall, the number of investment facilitation measures adopted by countries over the past six years remains relatively low compared with the numbers of other investment promotion measures. In addition, only about 20 per cent of the 111 investment laws analyzed by UNCTAD deal with specific aspects o ...

Rating Action: Moody`s affirms HMN Naturgas I/S Aaa debt rating

... MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001 ...

... MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001 ...

"Super Equivalent" Basel III Liquidity Coverage Ratio

... High-quality liquid assets (or HQLAs) generally consist of unencumbered assets free of transfer restrictions that are readily convertible into cash under periods of stress, or can generate sufficient liquidity through sale or secured borrowing. When characterizing assets as HQLAs, the federal bankin ...

... High-quality liquid assets (or HQLAs) generally consist of unencumbered assets free of transfer restrictions that are readily convertible into cash under periods of stress, or can generate sufficient liquidity through sale or secured borrowing. When characterizing assets as HQLAs, the federal bankin ...

Why were there fire sales of mortgage

... them. Therefore, these investors will only buy them if they sell at enough of a discount. With investors most knowledgeable about a class of securities sidelined, trade prices for these securities should vary considerably, after accounting for fundamentals, as there would only be weak forces pushing ...

... them. Therefore, these investors will only buy them if they sell at enough of a discount. With investors most knowledgeable about a class of securities sidelined, trade prices for these securities should vary considerably, after accounting for fundamentals, as there would only be weak forces pushing ...

Credit Expansion and Neglected Crash Risk * Matthew Baron

... this contrast indicates two different types of sentiment—credit expansions are associated with neglect of tail risk, while low dividend yield is associated with optimism about the overall distribution of future economic fundamentals. Nevertheless, they are not independent predictors of the bank equi ...

... this contrast indicates two different types of sentiment—credit expansions are associated with neglect of tail risk, while low dividend yield is associated with optimism about the overall distribution of future economic fundamentals. Nevertheless, they are not independent predictors of the bank equi ...

Promotion of unregulated collective investment schemes

... scheme funds that are not structured as unregulated collective investment schemes are outside of the scope. A number of other arrangements which are fund like but do not take the form of a non mainstream pooled investment will therefore remain unaffected by the new rules. The FCA have also confirmed ...

... scheme funds that are not structured as unregulated collective investment schemes are outside of the scope. A number of other arrangements which are fund like but do not take the form of a non mainstream pooled investment will therefore remain unaffected by the new rules. The FCA have also confirmed ...

accounting standards and information: inferences from cross

... that the 2002 results from AXA are not unique. Across the other eighteen European financial firms shown in the table, the absolute value of the difference in net income ranges from -314 percent to +117 percent for the insurance companies and from -226 percent to +57 percent for the banks. The media ...

... that the 2002 results from AXA are not unique. Across the other eighteen European financial firms shown in the table, the absolute value of the difference in net income ranges from -314 percent to +117 percent for the insurance companies and from -226 percent to +57 percent for the banks. The media ...

The Impact of Collateral

... “Risk management of collateral has become more critical,” says Jennis. “Systems need to look at the type of collateral and what is accessible. They need reports in terms of concentration such as are available on GlobalCollateral’s Collateral Management Utility. They need to do it more frequently: da ...

... “Risk management of collateral has become more critical,” says Jennis. “Systems need to look at the type of collateral and what is accessible. They need reports in terms of concentration such as are available on GlobalCollateral’s Collateral Management Utility. They need to do it more frequently: da ...

Volatility and Premiums in US Equity Returns

... is greater than a year, the standard deviation of the average is less than the standard deviation of year-byyear annual returns. Table 2 shows that the standard deviation of the average equity premium drops from 17.85% for a one-year period to 7.98% for five years, 5.65% for ten years, 3.57% for 25 ...

... is greater than a year, the standard deviation of the average is less than the standard deviation of year-byyear annual returns. Table 2 shows that the standard deviation of the average equity premium drops from 17.85% for a one-year period to 7.98% for five years, 5.65% for ten years, 3.57% for 25 ...

Leveraged buyout

A leveraged buyout (LBO) is a transaction when a company or single asset (e.g., a real estate property) is purchased with a combination of equity and significant amounts of borrowed money, structured in such a way that the target's cash flows or assets are used as the collateral (or ""leverage"") to secure and repay the borrowed money. Since the debt (be it senior or mezzanine) has a lower cost of capital (until bankruptcy risk reaches a level threatening to the lender[s]) than the equity, the returns on the equity increase as the amount of borrowed money does until the perfect capital structure is reached. As a result, the debt effectively serves as a lever to increase returns-on-investment.The term LBO is usually employed when a financial sponsor acquires a company. However, many corporate transactions are partially funded by bank debt, thus effectively also representing an LBO. LBOs can have many different forms such as management buyout (MBO), management buy-in (MBI), secondary buyout and tertiary buyout, among others, and can occur in growth situations, restructuring situations, and insolvencies. LBOs mostly occur in private companies, but can also be employed with public companies (in a so-called PtP transaction – Public to Private).As financial sponsors increase their returns by employing a very high leverage (i.e., a high ratio of debt to equity), they have an incentive to employ as much debt as possible to finance an acquisition. This has, in many cases, led to situations, in which companies were ""over-leveraged"", meaning that they did not generate sufficient cash flows to service their debt, which in turn led to insolvency or to debt-to-equity swaps in which the equity owners lose control over the business and the debt providers assume the equity.