NBER WORKING PAPER SERIES WHAT DOES FUTURES

... financial markets, which causes asset prices to initially underreact to news. This assumption has been used successfully in a variety of contexts including macroeconomics (Mankiw and Reis, 2002), international finance (Gourinchas and Tornell, 2004), and financial economics (Hong and Stein, 1999). Hong ...

... financial markets, which causes asset prices to initially underreact to news. This assumption has been used successfully in a variety of contexts including macroeconomics (Mankiw and Reis, 2002), international finance (Gourinchas and Tornell, 2004), and financial economics (Hong and Stein, 1999). Hong ...

The Behavior of US Interest Rate Swap Spreads in Global Financial

... Four determinants of swap spreads - default risk, the slope of yield curve, liquidity premium and volatility - are chosen. As for default risk, two kinds of default risk are used to investigate the sensitivity of swap spreads to Aaa and Baa corporate bond spreads. An interest rate swap is an agreeme ...

... Four determinants of swap spreads - default risk, the slope of yield curve, liquidity premium and volatility - are chosen. As for default risk, two kinds of default risk are used to investigate the sensitivity of swap spreads to Aaa and Baa corporate bond spreads. An interest rate swap is an agreeme ...

Preview - American Economic Association

... sector. When more investors choose to become dealers, the price dispersion among interdealer trades is larger (i.e., the dispersion ratio is higher), and customers’ transactions tend to go through more layers of dealers (i.e., the chain is longer). Our model implies that both the dispersion ratio an ...

... sector. When more investors choose to become dealers, the price dispersion among interdealer trades is larger (i.e., the dispersion ratio is higher), and customers’ transactions tend to go through more layers of dealers (i.e., the chain is longer). Our model implies that both the dispersion ratio an ...

Anatomy of a Bond Futures Contract Delivery Squeeze

... 15 years eligible for delivery. On LIFFE, for the March 1998 Long Gilt contract, eligible gilts include those issues with between 10 years to 15 years to maturity. The short decides which bond to deliver (the quality option), and also when to deliver during the delivery month (the timing option). Th ...

... 15 years eligible for delivery. On LIFFE, for the March 1998 Long Gilt contract, eligible gilts include those issues with between 10 years to 15 years to maturity. The short decides which bond to deliver (the quality option), and also when to deliver during the delivery month (the timing option). Th ...

World Financial Markets, 1900-1925

... I present a new dataset that describes the financial markets of the early twentieth century. Historical data have proven useful to better understand how financial markets operate. Estimation of the equity-premium (e.g. Goetzmann and Ibbotson (2006)), the efficiency of derivatives markets (Moore and J ...

... I present a new dataset that describes the financial markets of the early twentieth century. Historical data have proven useful to better understand how financial markets operate. Estimation of the equity-premium (e.g. Goetzmann and Ibbotson (2006)), the efficiency of derivatives markets (Moore and J ...

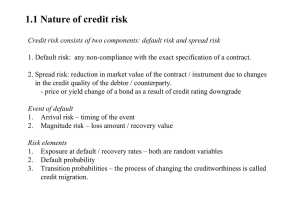

Default risk and spread risk

... rescheduling of payments on any external indebtedness. In practice, bankruptcy corresponds to the situation where the firm is liquidated, and the proceeds from the asset sale is distributed to the various claim holders according to pre-specified priority rules. ...

... rescheduling of payments on any external indebtedness. In practice, bankruptcy corresponds to the situation where the firm is liquidated, and the proceeds from the asset sale is distributed to the various claim holders according to pre-specified priority rules. ...

Chapter 1: An Introduction to Corporate Finance

... Booth/Cleary Introduction to Corporate Finance, Second Edition ...

... Booth/Cleary Introduction to Corporate Finance, Second Edition ...

Determinants of stock-bond market comovement in the Eurozone

... attempts to indentify the economic factors driving their time-series behavior. During the last decade, may academic studies have examined the dynamic relationship between stock and bond returns (e.g. de Goeij and Marquering, 2004, Cappiello et al., 2006, Connolly et al, 2007). One of the most promin ...

... attempts to indentify the economic factors driving their time-series behavior. During the last decade, may academic studies have examined the dynamic relationship between stock and bond returns (e.g. de Goeij and Marquering, 2004, Cappiello et al., 2006, Connolly et al, 2007). One of the most promin ...

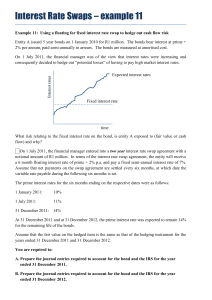

Interest Rate Swaps – example 11

... i.e the total net cash flow (received less paid) is expected to be nil. However the market interest rates will inevitably move differently to the expectations of the issuing entity (bank). Consequently the fair value of the swap is calculated at year end and approximates the present value of expecte ...

... i.e the total net cash flow (received less paid) is expected to be nil. However the market interest rates will inevitably move differently to the expectations of the issuing entity (bank). Consequently the fair value of the swap is calculated at year end and approximates the present value of expecte ...

Presentation title here in Arial 32pt

... is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Schroders has expressed its own views and opinions in this document and these may change. Information herein is believed to be reliable but Schroder Investment Management Ltd (SIM) does not warrant its ...

... is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Schroders has expressed its own views and opinions in this document and these may change. Information herein is believed to be reliable but Schroder Investment Management Ltd (SIM) does not warrant its ...

Telefónica, SA

... volume-weighted average price of the TELEFÓNICA shares on the Spanish Securities Markets in the trading sessions between March 3 and 16, 2016 (both inclusive), as described in the terms and conditions of the Bonds, which was 9.9346 euros. This reference price is equal to the exercise price of the ca ...

... volume-weighted average price of the TELEFÓNICA shares on the Spanish Securities Markets in the trading sessions between March 3 and 16, 2016 (both inclusive), as described in the terms and conditions of the Bonds, which was 9.9346 euros. This reference price is equal to the exercise price of the ca ...

Download attachment

... The development of a debt securities market is an important initial step towards the formation of the basic rudimentary structure of the capital market. It is an important way of attracting both domestic and international funds should be high priority on the agenda of SADC Stock Exchanges, Committee ...

... The development of a debt securities market is an important initial step towards the formation of the basic rudimentary structure of the capital market. It is an important way of attracting both domestic and international funds should be high priority on the agenda of SADC Stock Exchanges, Committee ...

12-1

... appropriate returns on non-financial assets • Lessons from capital market history • There is a reward for bearing risk • The greater the potential reward, the greater the risk • This is called the risk-return trade-off ...

... appropriate returns on non-financial assets • Lessons from capital market history • There is a reward for bearing risk • The greater the potential reward, the greater the risk • This is called the risk-return trade-off ...

semester v cm05bba05 – investment management

... d. None of the above 76. …………….. is an organized market for trading securities a. Stock exchange b. Primary market c. New issue market d. None of the above 77. Carry over the transactions /settlement of share purchase to the next day is called ………………. a. Badla b. Call c. Spot delivery d. Hand delive ...

... d. None of the above 76. …………….. is an organized market for trading securities a. Stock exchange b. Primary market c. New issue market d. None of the above 77. Carry over the transactions /settlement of share purchase to the next day is called ………………. a. Badla b. Call c. Spot delivery d. Hand delive ...

Secondary Market Regulations of Government Bonds

... Trading in response to an interest rate decline An interest rate declines Get the initial investment back and a CAPITAL GAIN Reinvest them in a new opportunity for the remaining maturity How much do the total returns improve? NOTHING! ...

... Trading in response to an interest rate decline An interest rate declines Get the initial investment back and a CAPITAL GAIN Reinvest them in a new opportunity for the remaining maturity How much do the total returns improve? NOTHING! ...

pdf The Treasury press release on the placement of BTp Italia

... definitive annual (real) coupon rate is set at 0.40%, paid on a semi-annual basis. The settlement date coincides with the accrual date. The amount issued has been of 8,014.368 million Euros and it coincides with the total turnover of valid purchase contracts concluded at par on the MOT (the Borsa It ...

... definitive annual (real) coupon rate is set at 0.40%, paid on a semi-annual basis. The settlement date coincides with the accrual date. The amount issued has been of 8,014.368 million Euros and it coincides with the total turnover of valid purchase contracts concluded at par on the MOT (the Borsa It ...

This paper is not to be removed from the Examination Halls

... Suppose a competitive risk neutral market maker clears the market by offering bid and ask quotes at which she is willing to trade one share of a stock. Traders are either uninformed noise traders who are as willing to buy a share as sell a share of the stock, or informed traders who know exactly the ...

... Suppose a competitive risk neutral market maker clears the market by offering bid and ask quotes at which she is willing to trade one share of a stock. Traders are either uninformed noise traders who are as willing to buy a share as sell a share of the stock, or informed traders who know exactly the ...

Treasury Terminology

... example is a forward contract in foreign exchange in which the purchase/sale of a currency for a future date is fixed today. The forward contract is “derived” and exists because of spot transactions between the two currencies, that is, the existence of a spot (cash) market, which is a fundamental co ...

... example is a forward contract in foreign exchange in which the purchase/sale of a currency for a future date is fixed today. The forward contract is “derived” and exists because of spot transactions between the two currencies, that is, the existence of a spot (cash) market, which is a fundamental co ...

Problem set 11 - The University of Chicago Booth School of Business

... and the correlation of +1 or +1 with +1 is zero. How does the presence of NL affect the optimal portfolio allocation between stocks and bonds? (There are two components, “market timing” and “optimal hedging.” Comment on both.) 7. Using standard statistics, long term bonds look like terrible in ...

... and the correlation of +1 or +1 with +1 is zero. How does the presence of NL affect the optimal portfolio allocation between stocks and bonds? (There are two components, “market timing” and “optimal hedging.” Comment on both.) 7. Using standard statistics, long term bonds look like terrible in ...

Lecture 8

... currency which is different from the home currency of the investor. • The bond will NOT be offered in the capital market of the country whose currency it is denominated in. • Example: A Chinese company issuing a U.S. dollar denominated bond in Japan. This bond will NOT be issued in the United States ...

... currency which is different from the home currency of the investor. • The bond will NOT be offered in the capital market of the country whose currency it is denominated in. • Example: A Chinese company issuing a U.S. dollar denominated bond in Japan. This bond will NOT be issued in the United States ...

Introduction of Mega Solar Project Bond Trust

... 2. Opportunities for institutional investors to have direct exposure to infrastructure projects Rated securities are easier to invest for capital markets investors Many Japanese investors’ exposure to JGBs and Muni bonds are too high and alternative long term investment opportunities are extreme ...

... 2. Opportunities for institutional investors to have direct exposure to infrastructure projects Rated securities are easier to invest for capital markets investors Many Japanese investors’ exposure to JGBs and Muni bonds are too high and alternative long term investment opportunities are extreme ...

ch.11

... Click the Return button in a feature to return to the main presentation. Click the Economics Online button to access online textbook features. Click the Reference Atlas button to access the Interactive Reference Atlas. Click the Exit button or press the Escape key [Esc] to end the chapter slide show ...

... Click the Return button in a feature to return to the main presentation. Click the Economics Online button to access online textbook features. Click the Reference Atlas button to access the Interactive Reference Atlas. Click the Exit button or press the Escape key [Esc] to end the chapter slide show ...