short-run supply curve

... • Economies or diseconomies of scale determine the shape of the long-run average total cost curve for individual firms. • When all firms in an industry expand, this new demand for raw materials and labor may push up the price of some inputs. When this happens, it gives rise to an increasing cost ind ...

... • Economies or diseconomies of scale determine the shape of the long-run average total cost curve for individual firms. • When all firms in an industry expand, this new demand for raw materials and labor may push up the price of some inputs. When this happens, it gives rise to an increasing cost ind ...

Test 5 - Competitive supply.tst

... Determine the market equilibrium price for this type of carpet. Also determine the production rate in the market. b. Determine how much the typical firm will produce per week at the equilibrium price. c. If all firms had the same cost structure, how many firms would compete at the equilibrium price ...

... Determine the market equilibrium price for this type of carpet. Also determine the production rate in the market. b. Determine how much the typical firm will produce per week at the equilibrium price. c. If all firms had the same cost structure, how many firms would compete at the equilibrium price ...

Pindyck/Rubinfeld Microeconomics

... producer is a price taker, the buyer’s demand for an input is given by the marginal revenue product curve. The MRP curve falls because the marginal product of labor falls as hours of work increase. When the producer of the product has monopoly power, the demand for the input is also given by the MRP ...

... producer is a price taker, the buyer’s demand for an input is given by the marginal revenue product curve. The MRP curve falls because the marginal product of labor falls as hours of work increase. When the producer of the product has monopoly power, the demand for the input is also given by the MRP ...

02 Demand and Supply: The Basics of the Market Economy

... that key factors like the quality of the team, the back on the number of college courses you take cost of the concessions, and the ease of traveling to at a time. the arena don’t change when the price goes up or Keep in mind that the law of demand is a gendown. This assumption is called ceteris pari ...

... that key factors like the quality of the team, the back on the number of college courses you take cost of the concessions, and the ease of traveling to at a time. the arena don’t change when the price goes up or Keep in mind that the law of demand is a gendown. This assumption is called ceteris pari ...

Pindyck/Rubinfeld Microeconomics

... producer is a price taker, the buyer’s demand for an input is given by the marginal revenue product curve. The MRP curve falls because the marginal product of labor falls as hours of work increase. When the producer of the product has monopoly power, the demand for the input is also given by the MRP ...

... producer is a price taker, the buyer’s demand for an input is given by the marginal revenue product curve. The MRP curve falls because the marginal product of labor falls as hours of work increase. When the producer of the product has monopoly power, the demand for the input is also given by the MRP ...

hanoi university

... “Investment trust” is a company which invests its money in other companies’ shares and makes profits from these investments. By 1929, investment trusts became very popular with investors in Wall Street. They sold stocks at higher prices than the value of the underlying stocks; therefore, the 1929 st ...

... “Investment trust” is a company which invests its money in other companies’ shares and makes profits from these investments. By 1929, investment trusts became very popular with investors in Wall Street. They sold stocks at higher prices than the value of the underlying stocks; therefore, the 1929 st ...

ECON 6070-001 MA Microeconomics

... Course description: Microeconomics is about what goods get produced and bought, and at what prices. The course teaches the mathematical structure of microeconomic theory. It is designed for first-year MA students. The formulation of the consumer's and the firm's problems is rigorously analyzed. Pric ...

... Course description: Microeconomics is about what goods get produced and bought, and at what prices. The course teaches the mathematical structure of microeconomic theory. It is designed for first-year MA students. The formulation of the consumer's and the firm's problems is rigorously analyzed. Pric ...

Consumer and producer surplus Consumer Surplus

... Consumers pay price P1 and demand a quantity of Q1. This is shown by area P10Q1X.The total benefit to the consumer is area 0Q1XY, but because they pay price P10Q1X, the net gain to the consumer P1XY, the shaded triangle. This is consumer surplus. It is always the area above market price and below th ...

... Consumers pay price P1 and demand a quantity of Q1. This is shown by area P10Q1X.The total benefit to the consumer is area 0Q1XY, but because they pay price P10Q1X, the net gain to the consumer P1XY, the shaded triangle. This is consumer surplus. It is always the area above market price and below th ...

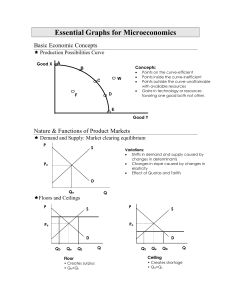

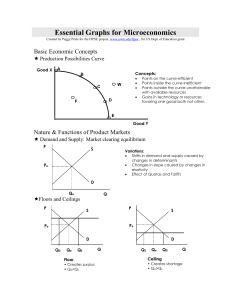

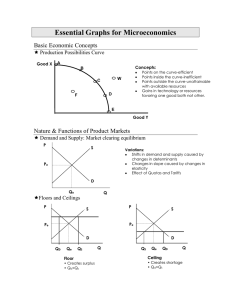

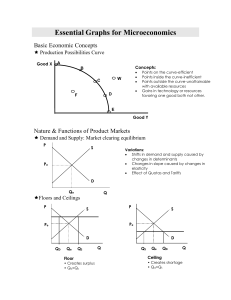

Essential Graphs for Microeconomics

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

Essential Graphs for Microeconomics

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

HOMEWORK 1 (Demand and Supply) ECO41 FALL 2011 UDAYAN

... This homework assignment tests your understanding of the theory of supply and demand. Any textbook on the principles of economics will cover this material. See for example my PowerPoint lecture notes and “additional material” on “supply and demand” on this course’s web site. This homework assignment ...

... This homework assignment tests your understanding of the theory of supply and demand. Any textbook on the principles of economics will cover this material. See for example my PowerPoint lecture notes and “additional material” on “supply and demand” on this course’s web site. This homework assignment ...

Demutualizing African Stock Exchanges: Challenges and

... opportunities presented by the demutualization movement for African stock exchanges. Traditionally, the ownership structure of a stock exchange was a mutually held organization. Members enjoy rights of ownership, decision-making (one-member, one vote) and trading. Demutualization is the term that de ...

... opportunities presented by the demutualization movement for African stock exchanges. Traditionally, the ownership structure of a stock exchange was a mutually held organization. Members enjoy rights of ownership, decision-making (one-member, one vote) and trading. Demutualization is the term that de ...

Essential Graphs for Microeconomics - pm

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

... MRP is the increase in total revenue resulting from the use of each additional variable input (like labor). The MRP curve is the resource demand curve. Location of curve depends on the productivity and the price of the product. MRP=MP x P MRC is the increase in total cost resulting from the employme ...

Chapter 2

... • Can predict either the direction in which price changes or the direction in which quantity changes, but not both • The change in equilibrium price or quantity is said to be indeterminate when the direction of change depends on the relative magnitudes by which demand & supply ...

... • Can predict either the direction in which price changes or the direction in which quantity changes, but not both • The change in equilibrium price or quantity is said to be indeterminate when the direction of change depends on the relative magnitudes by which demand & supply ...

Managerial Economics - Ramkhamhaeng University

... • Can predict either the direction in which price changes or the direction in which quantity changes, but not both • The change in equilibrium price or quantity is said to be indeterminate when the direction of change depends on the relative magnitudes by which demand & supply ...

... • Can predict either the direction in which price changes or the direction in which quantity changes, but not both • The change in equilibrium price or quantity is said to be indeterminate when the direction of change depends on the relative magnitudes by which demand & supply ...

CAPM and APT - BYU Marriott School

... CAPM (continued) Why is it important? • It provides a benchmark rate of return for evaluating possible investments, and identifying potential mis-pricing of investments • For example, an analyst might want to know whether the expected return she forecast is more or less than its “fair” market ret ...

... CAPM (continued) Why is it important? • It provides a benchmark rate of return for evaluating possible investments, and identifying potential mis-pricing of investments • For example, an analyst might want to know whether the expected return she forecast is more or less than its “fair” market ret ...

The Long-Run Industry Supply Curve

... 6. The long-run industry supply curve is often horizontal. It may slope upward if there is limited supply of an input. It is always more elastic than the short-run industry supply curve. 7. In the long-run market equilibrium of a competitive industry, profit maximization leads each firm to produce ...

... 6. The long-run industry supply curve is often horizontal. It may slope upward if there is limited supply of an input. It is always more elastic than the short-run industry supply curve. 7. In the long-run market equilibrium of a competitive industry, profit maximization leads each firm to produce ...

Price ceilings and floors

... market forces establish equilibrium prices and quantities. While equilibrium conditions may be efficient, not everyone will be satisfied with prevailing market price (either too high or too low) Price controls are usually implemented when it is perceived that the market price is unfair to either ...

... market forces establish equilibrium prices and quantities. While equilibrium conditions may be efficient, not everyone will be satisfied with prevailing market price (either too high or too low) Price controls are usually implemented when it is perceived that the market price is unfair to either ...

Monopoly - Helena Glebocki Keefe

... • People in US do not fly to Europe to buy their medicine • Two markets are separate ...

... • People in US do not fly to Europe to buy their medicine • Two markets are separate ...