Chapter 3: Over-the-Counter Derivatives

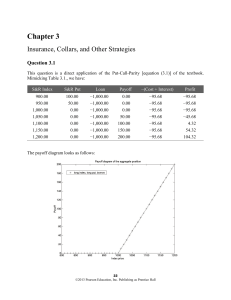

Chapter 3

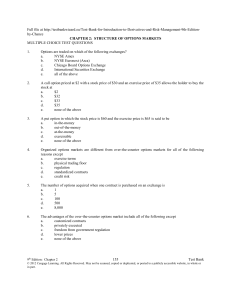

chapter 2: the structure of options markets

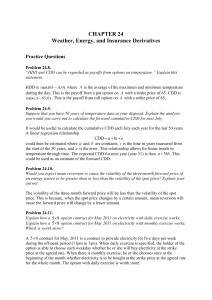

Chapter 24

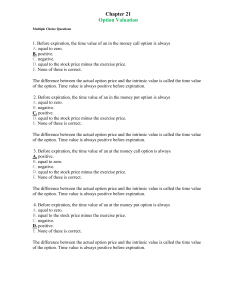

Chapter 21 Option Valuation

Chapter 20

Chapter 1: Intro to Derivatives

Chapter 17

CHAPTER 16 Futures Contracts

chapter 16

Chapter 15

CHAPTER 13 Options on Futures

chapter 12: swaps

Chapter 12 Balance of Payments Accounting

Chapter 10

Chap024

ch11 - U of L Class Index

Ch 7: 1.1-4

CGZ CGF CGB

Catastrophe Insurance Products in Markov Jump Diffusion Model