Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

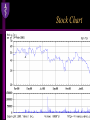

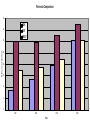

Stock Analysis: Feb. 15, 2001 Joel Bauman Nokia Oyj (NOK) Company Overview • Leading worldwide supplier of mobile phones and a leader in the supply of mobile, fixed and IP networks. • Listings on six major exchanges. • Founded in 1865 in Finland as a paper milling co. • First entered telecommunications in 1960 • Streamlined company during 1990s to focus on telecommunications. Company History Continued • Cellular network since 1981 • First transportable phone, 1984: weighed 4.8 kilos • Divesting successfully since 1992 • 1995,96: sold off cable and tv industries • Went public in 1995 (on NYSE) • Pioneered GSM (global system for mobile comm. As of 1997, 59 agreements in 31 countries Trendy Handsets • Emphasis on personal technology of personal communication: DESIGN • Innovated large graphic display, ringing tones, colored covers, battery signals, etc. • Simplicity and Style: Highly standardized products good for production, too • Significant economy of scale--at least 2 times that of nearest competitor (MOT) • 18 new phone models in 1999 alone Acquisitions • At least 4 major divisions: Internet Communications, Networks, Mobile Phones, Communication Products • All of which have been gobbling up companies increasingly in past 3 years, for enhancing IP networks & telephony, broadband • 15 acquisitions, 6 divestures • Some have been expensive: $335M for Network Alchemy Financial Overview • FY 2000, sales rose 54% to EUR30.38 billion. Revenues reflect order inflow in Nokia Networks and increased sales of Nokia Mobile Phones. • Net income rose 53% to EUR3.94 billion. Earnings reflect higher operating margins. • Total of 60,000 employees; little outsourcing • In 1999, sold products in over 130 countries Wireless Warriors Q4 2000 Numbers NOK Revenues 9.284B Gross Income 3.342B Net Income 1.204B Gross Margins 36.0% Net Margins 13.0% R&D Budget 764M R&D Percent 8.3% Market Capitalization $139.2B MOT $7.736B $3.135B $0.199B 40.5% 2.6% $815M 10.5% $42.44B ERICY $8.327B $1.927B $0.228B 23.1% 2.7% $1365M 16.4% $77.06B Prospects for 2001 • Revised forecast = 23-36 % growth, rather than projected 45% growth in 2000 • Continued product launches: GPRS (2.5G) by 3rd quarter (rudimentary internet); 3G a year later; R&D continues at 8.5% sales • Some outsourcing to cutback on costs (800 jobs recently cut in Texas--compare with MOT and ERICY) • Stock target price: $42 (revised from $55) Branding • Ranked the #5 most valuable worldwide brand in 2000 at $38.5B. (KO #1, MSFT #2, IBM #3, INTC #4, GE #6, F #7, DIS #8, MCD #9, T #10) • Up 86% from 1999 ($20.6B); ranked higher than AT&T (#10) and Motorola (#49) • Popular and recognizable ring • Sugar Bowl game sponsorship Networking • New network contracts within the past two weeks alone include ventures into Bolivia (GRPS--general packet radio service) and Hong Kong (TETRA--Terrestrial truncated radio system). Also, Venezuela. • First nationwide TETRA system implemented in Finland--will gradually replace existing radio networks--good for government/military purposes • Nokia Telelcommunications changed its name to Nokia Networks a couple of years ago. Market Share • Currently 32% of all handsets sold • Twice that of Motorola and 3 times that of Ericsson • Plans to increase share to 35% by end of year, if not higher, even though sales esimates expected to decrease from 550M to 500M units. 1 billion handset sales by the end of 2002. Recent Analysis • 12-Feb-01 Wit SoundView upgrade: from Buy to Strong Buy • 30-Jan-01 Raymond James downgrade from Strong Buy to Mkt Perform • Salomon Smth Brny downgrade: from Outperform to Neutral • 23-Jan-01 Dresdner Klnwrt Bnsn downgrade from Reduce to Sell • 19-Jan-01Mrgn Stnly Dn Wttr downgrade: from Outperform to Neutral • 18-Jan-01 JP Morgan initiated: at Buy • 5-Jan-01 Dain Rauscher Wessels initiated: at Buy Aggressive • 19-Oct-00 Chase H&Q upgrade: from Buy to Strong Buy • 18-Oct-00 First Union Sec downgrade:from Strong Buy to Buy • 13-Sep-00 Sands Brothers initiated: at Buy Current Recommendations • Despite downgrades, 23 out of 26 analysts recommend NOK as either a strong or moderate buy. • No one recommends sell --taken from Yahoo! Finance “research” option Stock Chart Stock Quote NOKIA CORP (NYSE:NOK) - More Info: News , Msgs , Profile , Research , Insider , Options Last Trade Change Prev Cls Volume Div Date 2:33PM · 29.70 +1.47 (+5.21%) 28.23 15,438,700 Apr 10, 2000 Day's Range 28.5 - 29.75 52-week Range 26.4900 - 62.5000 Bid N/A Ask N/A Open 0.00 Earn/Shr P/E Mkt Cap 0.76 37.14 139.2B Avg Vol 13,619,545 Ex-Div Apr 11, 2000 Div/Shr 0.19 Yield 0.68 1 Year Relative Performance 1 Year Relative Performance Valuation Share Price 2000 EPS 2001 EPS NOK $29.51 $0.73 $0.88 MOT $19.44 $0.84 $0.83 ERICY $9.81 $0.17 $0.25 Dividends Yield P/E (2000) $0.19 0.68% 40.4 $0.16 0.84% 23.1 $0.06 0.61% 57.7 P/E (2001) 5 Yr Earn Grow PEG (2001) 33.5 26.8% 1.25 23.4 18.5% 1.26 39.4 24.9% 1.58 Valuation Continued Share Price Price/Book Price/Sales NOK $29.51 14.92 4.86 MOT $19.44 2.23 1.15 ERICY $9.81 8.60 2.47 Current Ratio Debt/Equity Return on Assets 1.47 0.14 24.34% 1.22 0.57 3.05% 1.32 0.05 9.35% Return on Equity 47.67% 6.59% 25.76% Return Equity = Effectiveness of management in using retained net income and turning it into additional net income. Revenue Comparison 40 NOK 35 MOT ERICY Billions of Dollars 30 25 20 15 10 5 0 1997 1998 1999 Year 2000 Earnings Per Share Comparison 1 NOK MOT ERICY 0.8 Earnings Per Share in Dollars 0.6 0.4 0.2 0 1997 1998 1999 -0.2 -0.4 -0.6 -0.8 Year 2000 Why Buy? • At a P/E of 37, NOK seems to be heavily undervalued compared to the rest of the Telecom sector, which has an average P/E of 100 • Bottom Fishing? 52 week low occurred yesterday during trading. Review • • • • Industry leader and pioneer Strong sales, earnings growth Global expansion Two-pronged attack: mobile phones and networks (fixed, mobile, and IP) • Keen sense of consumer and business trends • Possibly undervalued company due to investor anxiety over recent growth Caution • Warned that will not meet first quarter growth expectations--but is 35% so bad?!? • Penetrance rate in Europe = 60%, much higher in Scandinavia • Growth from replacement phones not as fast as anticipated--data traffic (2nd gen) phones unnecessary if applications and networks not up to date • New competition from Siemens, Sony The Future • Short term: Aggressive take over of market share from Motorola, Ericsson; only one left standing in 3 years • Concentrate on network infrastructure until data traffic becomes realistic option. • Long term: commitment to broadband solutions, wireless data applications, increasingly user-friendly mobile devices and third-generation mobile telephony