Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

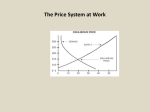

Chapter 21.3 Markets and Prices Supply and Demand at Work • Markets bring buyers and sellers together. The forces of supply and demand work together in markets to establish prices. In our economy, prices form the basis of economic decisions. See graph pg. 472. • A surplus is the amount by which the quantity supplied is higher than the quantity demanded. On the graph, it appears as the horizontal distance between the supply and demand curves at any point above where the curves cross. continued • A surplus signals that the price is too high. At that price, consumers will not buy all of the product that suppliers are willing to supply. In a competitive market, a surplus will not last. Sellers will lower their price to sell their goods. • A shortage is the amount by which the quantity demanded is higher than the quantity supplied. On the graph, it appears as the horizontal distance between the supply and demand curves at any point below where the curves cross. continued • A shortage signals that the price is too low. At that price, suppliers will not supply all of the product that consumers are willing to buy. In a competitive market, a shortage will not last. Sellers will raise there price. continued • When operating without restriction, our market economy eliminates shortages and surpluses. Over time, a surplus forces the price down and a shortage forces the price up until supply and demand are balanced. The point where they achieve balance is the equilibrium price. At this price, neither a surplus nor a shortage exists. continued • Once the market price reaches equilibrium, it tends to stay there until either supply or demand changes. When that happens, a temporary surplus or shortage occurs until the price adjusts to reach a new equilibrium price. continued • Sometimes the gov’t sets the price of a product because it believes the forces of supply and demand are unfair. A price ceiling is a gov’t-set maximum price that can be charged for a good or a service. A price floor is a gov’t-set minimum price that can be charged for a good or service. Prices as Signals • Prices are signals that help businesses and consumers make decisions. They also help answer the basic economic questions. • Consumers’ purchases help producers decide WHAT to produce. Producers focus on goods and services that consumers are willing to buy prices that yield a profit. continued • Prices help businesses and consumers decide HOW to produce. To stay in business, a supplier must find a way to provide a good or service at a price consumers will pay. • Prices help businesses and consumers decide FOR WHOM to produce. Some businesses aim their products at a small number of consumers who will pay higher prices. Others try to sell to larger numbers of people who want to spend less. continued • Consumers look for the best value for what they spend. Producers seek the best price and profit for what they have to sell. The information that prices provide allows people to work together to produce more of the things people want. • Prices favor neither producer nor consumer. They are a compromise that results from competition between buyers and sellers. The more competitive the market, the more efficient the price adjustment process. continued • Prices are flexible. Unforeseen events affect supply and demand. Buyers and sellers react to the new level of prices by adjusting their consumption and production. Soon, the system is functioning smoothly again. • The price system provides for freedom of choice. A market economy provides consumers a variety of products and prices from which to choose. continued • In command economies, gov’t planners decide how much of each product to produce and limit the product’s variety. Products are offered at artificially low prices, but seldom are enough produced to satisfy everyone. • Prices are familiar. People can make buying decisions quickly and efficiently because they know exactly how much they would have to pay for the product.