Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

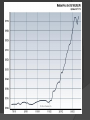

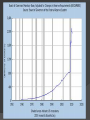

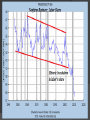

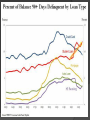

Fed Lowered rates 2001 Average home buyer was becoming speculator 2005 Institutions wanted higher return 2003 Money was being thrown at originators 2004 Loan guidelines not enforced Some builders began to offer 100k cash back, pay off debt 2006 Whole subdivisions were wiped out 2006-2007 Spilled into resale market 2006-2007 Ponzi schemes and scams began to unravel 2007 These values were used by the average homeowner to Refinance The cancer spreads Sub prime collapse Oct. 2007 No options left No government programs can help 2010 Market booms from tax credit Falls right back down again Pulled Demand Forward 2011 Buy Buy Buy State Policies Laws limit inventory Federal lower rates accounting changes $38 OF DEBT NOW $1 GDP QE HAS LOST ITS JUICE Government realized they must utilize this option Short sales are increasing by triple digits year over year Banks to take Real Time loss Short sales less of a loss and cost House not left empty Eliminates living units, artificial shortage All government programs will fail with out principal reduction Fed Admits Policy Causes “ ASSET BUBBLES” *WILLIAMS SAYS POLICY MAY YIELD ASSET BUBBLES, UNINTENDED RESULT *YELLEN : POLICY DOES HURT SAVERS *PAULSON: CURRENT POLICY WILL CAUSE CRISIS * SCHWAB: WE ARE IN A MANIPULATED MARKET BIGGEST DROP IN 40 YEARS! The Hedge Fund Landlord ERA Rental housing has long been a decentralized, locally owned industry No Mom and Pop real estate investor can compete with financial institutions who can borrow unlimited sums of money from the Federal Reserve at near-zero rates of interest At 4%, the price $400,000, with a 30% down of $120,000 and a mortgage of $280,000, and the mortgage accrues the same $11,200 in annual interest. Imagine being able to borrow $400,000 at 1% with zero collateral. You can now buy the rental property for cash, and pay only $4,000 in simple annual interest. Now multiply the $400,000 and the $7,000 by 1,000. Now you can buy $400,000,000 of rental properties and skim $7,000,000 in annual profits, . . . .