Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

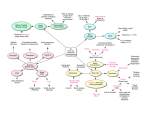

Expenditure & Budget Tracking Process COUNTRY: NIGERIA Overview of Immunization Expenditure Tracking Process in NIGERIA • • - Summary of existing country expenditure tracking process for the routine immunization program Appropriation/Financial Resource Requirements (FRR) Recording, analysis and reporting of expenditure Budget Performance Review Statutory Audit Dimensions of expenditure tracking Vouching & Journalizing expenditure, Preparation of Ledgers & Trial Balance Reporting of expenditure through the statutory financial statements, Audit of financial statement/report by the Auditor General and make recommendations to National/state Assembly Committee on Public Accounts (PAC), - PAC conduct thorough investigations into any case(s) of abuse or misappropriation with a view to recovering any funds lost. • Bottlenecks and solutions THE BUDGET CYCLE - OVERVIEW 5. BUDGET MONITORING & 1. MTSS/MTEF PREPARATION & APPROVAL EVALUATION -warrants/release of funds -monitoring 4. BBUDGET IMPLEMENTATION (Appropriation Act, budget announcement) 2. PREPARATION OF BUDGET PROPOSAL BY MDAs (using MTEF) 3. BUDGET PROPOSAL DEFENCE & APPROVAL (Ministry, Executive, Legislative) Expenditure Tracking at LGA/State/Federal Levels Existing mechanisms Responsibility 1. Collection & reporting of immunization expenditures at each level: Federal/State: The Director of Finance and Accounts, LGA: Treasurer of the Local Government 1. Mechanisms Reporting forms for capturing immunization expenditures include: • Vouchers, Departmental Vote Allocation book, Cashbook, Journal books and Ledgers. Aggregate expenditure is published in the Annual statutory financial statements. Immunization expenditure easily identified in records • Expenditures are reported separately since immunization exists as a separate line item in the annual appropriation Act. 3. Technology Reporting and analysis of immunization expenditures are conducted with PCs using Microsoft excel and other appropriate software • 4. Sources System distinguishes government from other immunization expenditures (domestic private, external) The annual statutory financial statements contain expenditure on government fund only. 5. Shared Costs No shared cost approach exists for vehicles and human resources 6. Frequency Expenditures are reported and analyzed at each level annually. WHO/UNICEF Joint Reporting Form (JRF) Process Some Issues to Consider 1. Importance. The annual JRF financial reports are the only direct measure of country immunization investments. 2. Responsibility Financial section of the WHO/UNICEF Joint Reporting Form (JRF) is completed by the ICC Finance Committee Review and submission to the WHO Country Office: Inter Agency Coordinating Committee (ICC) 3. Strategy Identification and compilation of public routine immunization expenditures is accomplished by collating expenditure returns from the national, states and local government/ward levels. Sources of expenditure data used include Paid vouchers, adjustment vouchers, Journal, ledger and Trial balance. 4. Under-reporting a. The current reporting system does not capture shared costs e.g. personnel cost. b. Can be resolved by apportioning costs using acceptable time ratios or number of immunization personnel at each level Sabin SIF budget flow analysis Some Issues to Consider • Purpose. To document and analyze annual immunization budget flows • Utility. Reveals bottlenecks in the annual budget execution, documents budget credibility. Provides unaudited information for empirical budgeting, advocacy, management improvement. • Users. MoH EPI teams. (Data are not externally reported.) • Frequency. Ideally performed each year. Sabin SIF budget flow analysis tool Country: Fiscal Year: Budget Processes Description Start: XXX Accounting concepts Amount in US$ End: XXX Local Currency exchange rate to US$ = 1 The initial projected immunization program budget (from current cMYP, amount of routine recurrent government projected costs, Spreadsheet 4. Financing) Projected government R.I. budget 2 The adjusted proposed immunization budget after review by the Ministry of Health, Council of Ministers or other budget review institution(s). The amount that was submitted for parliamentary approval. Immunization budget proposed by MOH 3 The final immunization budget that was approved by parliament. Immunization budget approved by parliament 4 Additional in-year funds approved for immunization. Any additional (supplemental) increases to the budget during the fiscal year. Total in-year immunization budget increase(s) approved by parliament Cash Hoarding 5 The amount of funds disbursed by Treasury to the Ministry of Health for immunization. Amount disbursed against approved immunization budget by Treasury to MOH Misclassification 6 Amount of funds in Box 5 actually allocated by the Ministry of Health to the immunization program. Amount of disbursed budget actually allocated to immunization program Budget Credibility Phase-IV: Expenditure 7 Amount of actual public routine immunization program expenditures. Includes expenditures against in-year supplementary budgets. Total immunization expenditures as of end fiscal year Phase-V: Reporting 8 Amount of government routine EPI expenditures reported for Indicator 6730 of the WHO/UNICEF Joint Reporting Form (JRF) for the reporting year. Phase-I: Proposed Budget Phase-II: Approved Budget Public Expenditure and Financing Accountability (PEFA) Framework Indicators PEFA Indicator Key Formula Guide [ ((Box 3 + Box 4) - Box 5) /(Box 3+ Box 4) ] x 100 [ (Box 5 - Box 6) / Box 5 ] x 100 Phase-III: Disbursement Absorptive Capacity Reporting Accuracy (Box 7 /(Box 3+ Box 4 ) x 100 (Box 7 / Box 6 ) x 100 If Box 7 > Box 8, then (Box 8/ Box 7) x 100 If Box 7 < Box 8, then (Box 7/ Box 8) x 100 Bottlenecks & Solutions • Areas for Improvement. • Timely implementation of budget cycle: delay in passing appropriation bill, cumbersome procurement procedures –delay in project excution • Tracking of sub-national expenditures needs improvement to be more robust and transparent • No cash backing and release of budgeted funds • Potential Solutions • Introducing public expenditure tracking survey, learning from ongoing pilot in Ekiti and Niger States. • Zero budgeting method as opposed to current incremental budgeting method • Bottom – up approach in planning, budgeting & tracking • Institute transparent and reproducible accounting system at all levels • Regular internal and external supervision • Transiting from paper based system to electronic system • Cash backing dependent on macroeconomic environment of the country. Implementing Authority (State and non State Actors) • Federal: Federal Ministry of Finance (Budget Office of the Federation), National Assembly, CSOs etc • State: Budget & Planning commission, State House of Assembly, CSOs, etc • LGA: Needs to introduce a tracking mechanism that will operate/function at this level • Health facility: Needs to introduce a tracking mechanism that will operate/function at this level INNOVATIONS • Introduction of Single Treasury Accounts (TSA) • Introduction of new planning horizon new budgeting technique (ZBB) • ZBB is a method of budgeting in which all expenses must be justified for each new period, (every year) Starts from a "zero base" Analyzes every function within an organization for its needs and costs Often builds budgets around what is needed for the upcoming year regardless of whether the budget is higher or lower than the previous one • Clearly linked to Government’s policy priorities • Allows top-level strategic goals to be linked to the budgeting process by • Tying them to specific functional areas of the organization, where Costs can be first grouped • ZBB is an improvement on the envelope system, • The flexibility of the concept allows for easy adaptation to country peculiarities INNOVATIONS • Introduction of Single Treasury Accounts (TSA) • Introduction of new planning horizon new budgeting technique (ZBB) • ZBB is a method of budgeting in which all expenses must be justified for each new period, (every year) Starts from a "zero base" Analyzes every function within an organization for its needs and costs Often builds budgets around what is needed for the upcoming year regardless of whether the budget is higher or lower than the previous one • Clearly linked to Government’s policy priorities • Allows top-level strategic goals to be linked to the budgeting process by • Tying them to specific functional areas of the organization, where Costs can be first grouped • ZBB is an improvement on the envelope system, • The flexibility of the concept allows for easy adaptation to country peculiarities Next Steps • Engagement of implementing authority to introduce proposed solution • Proper advocacy and sensitization of the relevant stakeholders with involvement of CSOs • Peer review mechanism for states (using the PHC scorecard) • Awareness creation through media and communication • Regular policy and technical briefs • Community sensitization to create demand for immunization services THANK YOU