Revised Guidance Statement GS 009: Auditing SMSFs

... the trust deed and applicable legislation. Complying SMSFs are eligible for tax concessions, and may also receive Superannuation Guarantee (SG) contributions. Complying SMSFs are Australian superannuation funds, which meet the requirements of the SISA and SISR and are “regulated”3 under the SISA. ...

... the trust deed and applicable legislation. Complying SMSFs are eligible for tax concessions, and may also receive Superannuation Guarantee (SG) contributions. Complying SMSFs are Australian superannuation funds, which meet the requirements of the SISA and SISR and are “regulated”3 under the SISA. ...

Does the Big-4 Effect Exist when Reputation and

... question of whether the Big-4 effect still exists when client-level and partner-level characteristics are held constant and when both the Big-4 firms and the non-Big-4 firms face low and similar litigation and reputational risks. This setting and our research design offer several advantages compare ...

... question of whether the Big-4 effect still exists when client-level and partner-level characteristics are held constant and when both the Big-4 firms and the non-Big-4 firms face low and similar litigation and reputational risks. This setting and our research design offer several advantages compare ...

Defence Audit Guidelines_Final 25 March 2010

... approaches to audit that can be applied by auditors for conducting the audit of government entities in Pakistan. FAM has been implemented in the Department of the Auditor-General of Pakistan (DAG). However, during the course of its implementation, it was found that though it is quite comprehensive f ...

... approaches to audit that can be applied by auditors for conducting the audit of government entities in Pakistan. FAM has been implemented in the Department of the Auditor-General of Pakistan (DAG). However, during the course of its implementation, it was found that though it is quite comprehensive f ...

The Effect of Audit Firm Specialization on Earnings Management

... monitoring role, an information role and an insurance role) (Wallace, 1981). How the auditor fulfils these roles determines the level of audit quality (Fernando et al., 2010). Audit quality is an important market performance measure in the market for audit services. The extent of industry-based expe ...

... monitoring role, an information role and an insurance role) (Wallace, 1981). How the auditor fulfils these roles determines the level of audit quality (Fernando et al., 2010). Audit quality is an important market performance measure in the market for audit services. The extent of industry-based expe ...

Yes, there is a big Difference between Audit on Profit Organizations

... sampling is often adopted in audits. In the case of financial audits, a set of financial statements are said to be true and fair when they are free of material misstatements - a concept influenced by both quantitative (numerical) and qualitative factors. Auditing is a vital part of accounting. Tradi ...

... sampling is often adopted in audits. In the case of financial audits, a set of financial statements are said to be true and fair when they are free of material misstatements - a concept influenced by both quantitative (numerical) and qualitative factors. Auditing is a vital part of accounting. Tradi ...

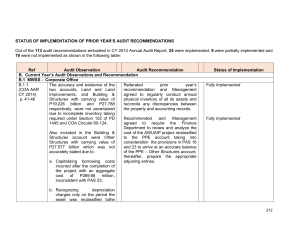

MWSS2015_Part3-Status_of_PY`s_Recomm

... B. Current Year’s Audit Observations and Recommendation B.1 MWSS - Corporate Office B.1.1 The accuracy and existence of the Reiterated prior year’s (COA AAR two accounts, Land and Land recommendation and Management CY 2014) Improvements, and Building & agreed to regularly conduct annual p. 41-46 Str ...

... B. Current Year’s Audit Observations and Recommendation B.1 MWSS - Corporate Office B.1.1 The accuracy and existence of the Reiterated prior year’s (COA AAR two accounts, Land and Land recommendation and Management CY 2014) Improvements, and Building & agreed to regularly conduct annual p. 41-46 Str ...

Notification 297/2015 dated 28th December, 2015 - Regarding the Internal Audit Manual (672 KB)

... designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. With commitment to integrity and acco ...

... designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. With commitment to integrity and acco ...

MANDATORY EMPHASIS PARAGRAPHS, CLARIFYING

... language. Specifically, when the audit report includes an emphasis paragraph that identifies and describes a critical audit matter, but does not describe specific audit procedures, clarifying the term reasonable assurance does not affect jurors’ negligence likelihood assessments of auditors. In con ...

... language. Specifically, when the audit report includes an emphasis paragraph that identifies and describes a critical audit matter, but does not describe specific audit procedures, clarifying the term reasonable assurance does not affect jurors’ negligence likelihood assessments of auditors. In con ...

Comprehensive Case A.1 – Enron

... independence can result in disciplinary action by regulators and/or professional organizations and litigation by those who relied on the financial statements (e.g., clients and investors). The profession, as a whole, depends on the value of independence in that the auditor’s opinion on the financial ...

... independence can result in disciplinary action by regulators and/or professional organizations and litigation by those who relied on the financial statements (e.g., clients and investors). The profession, as a whole, depends on the value of independence in that the auditor’s opinion on the financial ...

Auditor Liability and Professional Skepticism: A Look at Lehman

... the likely reasons why warranted levels of skepticism might be consciously or subconsciously suppressed by staff level auditors.6 Operationalizing skepticism is a challenge that the profession needs to address, since this rather abstract concept, calling for a certain attitude or perspective, must s ...

... the likely reasons why warranted levels of skepticism might be consciously or subconsciously suppressed by staff level auditors.6 Operationalizing skepticism is a challenge that the profession needs to address, since this rather abstract concept, calling for a certain attitude or perspective, must s ...

Competency area - Chartered Institute of Internal Auditors

... with senior management and confirming the level of assurance that particular audit work attracts (recognising, for example, that a light touch audit with little testing may provide a lower level of assurance than an audit that encompasses both compliance and substantive testing), and is able to prov ...

... with senior management and confirming the level of assurance that particular audit work attracts (recognising, for example, that a light touch audit with little testing may provide a lower level of assurance than an audit that encompasses both compliance and substantive testing), and is able to prov ...

Leading Practice Examples of Audit Committee Reporting

... • The Audit Committee Charter • The Internal Audit Department Charter • Committee members and their backgrounds focusing on any changes since last meeting • Prior Audit Committee Reports and Minutes • Any arrangements that have been documented concerning report content expectations ...

... • The Audit Committee Charter • The Internal Audit Department Charter • Committee members and their backgrounds focusing on any changes since last meeting • Prior Audit Committee Reports and Minutes • Any arrangements that have been documented concerning report content expectations ...

internal-auditing-instructional-material

... Work is to be adequately planned Assistants are to be properly supervised A review is to be made of compliance with applicable laws & regulation During the audit, a study and evaluation shall be made of internal control systemadmin control ) applicable to the organization program, activity, or funct ...

... Work is to be adequately planned Assistants are to be properly supervised A review is to be made of compliance with applicable laws & regulation During the audit, a study and evaluation shall be made of internal control systemadmin control ) applicable to the organization program, activity, or funct ...

Sample September / December 2015 answers

... the year end using the closing rate. Exchange gains and losses should be recognised within profit for the year. The risk is that the incorrect exchange rate is used for the translation and retranslation, or that the retranslation does not happen at the year end, in which case trade payables and prof ...

... the year end using the closing rate. Exchange gains and losses should be recognised within profit for the year. The risk is that the incorrect exchange rate is used for the translation and retranslation, or that the retranslation does not happen at the year end, in which case trade payables and prof ...

The Auditor - Whose Agent Is He Anyway

... framework would improve the quality of financial reporting. Failing this framework, Peasnell questions whether the auditing function would be a viable alternative for ‘organising and policing’ corporate disclosure. He describes how there are those who view external auditing as a largely useless lega ...

... framework would improve the quality of financial reporting. Failing this framework, Peasnell questions whether the auditing function would be a viable alternative for ‘organising and policing’ corporate disclosure. He describes how there are those who view external auditing as a largely useless lega ...

working program - Almaty Management University

... 1. Basic principles of sampling in the audit. 2. Stages of a spot check. 3. Determination of the data set (stratification) are sampled. 4. Methods of selection of samples (random and systematic). 5. Letter of commitment and the contract for audit 6. Preparation of the overall audit plan. Preparation ...

... 1. Basic principles of sampling in the audit. 2. Stages of a spot check. 3. Determination of the data set (stratification) are sampled. 4. Methods of selection of samples (random and systematic). 5. Letter of commitment and the contract for audit 6. Preparation of the overall audit plan. Preparation ...

Answers

... Testing cash controls at stores Currently the internal audit department undertake inventory counts at each of the stores. This role could be increased to include controls testing over cash receipts and cash counts. As a retailer the stores will have a significant amount of cash at each premise and w ...

... Testing cash controls at stores Currently the internal audit department undertake inventory counts at each of the stores. This role could be increased to include controls testing over cash receipts and cash counts. As a retailer the stores will have a significant amount of cash at each premise and w ...

Auditor`s Responsibility

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

Hang Chi Holdings Limited 恒智控股有限公司

... Responsibility and Duty The main responsibilities and duties of the Audit Committee should include: Relationship with the Company’s auditor 5.1 to act as the key representative body for overseeing the Company’s relations with the external auditor; 5.2 to be primarily responsible for making recomme ...

... Responsibility and Duty The main responsibilities and duties of the Audit Committee should include: Relationship with the Company’s auditor 5.1 to act as the key representative body for overseeing the Company’s relations with the external auditor; 5.2 to be primarily responsible for making recomme ...

Major Duties and Responsibilities of Assistant Manager (Audit)

... Palli Karma-Sahayak Foundation’s (PKSF) Internal Audit Department (IAD) is an independent department entrusts to conduct financial and management audit of its Partner Organizations (POs), which are directly implementing PKSF’s programs and projects at field level all over the country. IAD is also re ...

... Palli Karma-Sahayak Foundation’s (PKSF) Internal Audit Department (IAD) is an independent department entrusts to conduct financial and management audit of its Partner Organizations (POs), which are directly implementing PKSF’s programs and projects at field level all over the country. IAD is also re ...