Studies of Barrier Options and their Sensitivities

... either touch or not touch a specified barrier H before or on the expiry T . This also depends on whether the barrier is hit from above or from below and the period during which the underlying price is monitored for barrier hits. There are two broad types of barrier options: a kick-out option, which ...

... either touch or not touch a specified barrier H before or on the expiry T . This also depends on whether the barrier is hit from above or from below and the period during which the underlying price is monitored for barrier hits. There are two broad types of barrier options: a kick-out option, which ...

economics - SchoolRack

... In panel (a), the price is P1, the quantity supplied is Q1, and producer surplus equals the area of the triangle ABC. When the price rises from P1 to P2, as in panel (b), the quantity supplied rises from Q1 to Q2, and the producer surplus rises to the area of the triangle ADF. The increase in produc ...

... In panel (a), the price is P1, the quantity supplied is Q1, and producer surplus equals the area of the triangle ABC. When the price rises from P1 to P2, as in panel (b), the quantity supplied rises from Q1 to Q2, and the producer surplus rises to the area of the triangle ADF. The increase in produc ...

On estimating the risk-neutral and real

... and lower matrices separated by the middle-most row both satisfy that their diagonals are equal, independently of each other. ...

... and lower matrices separated by the middle-most row both satisfy that their diagonals are equal, independently of each other. ...

Hedging Barrier Options - Institute for Advanced Studies (IHS)

... In contrast, when claims cannot be perfectly replicated by trading marketable assets, any hedging strategy leaves some residual risk and investors' attitudes toward risk a ect the pricing of the claims. For example, Hull and White (1987) introduce stochastic volatility in a model otherwise similar t ...

... In contrast, when claims cannot be perfectly replicated by trading marketable assets, any hedging strategy leaves some residual risk and investors' attitudes toward risk a ect the pricing of the claims. For example, Hull and White (1987) introduce stochastic volatility in a model otherwise similar t ...

0224 - European Financial Management Association

... The payoff of equities is linear and additive so that the payoff of a portfolio of equities is also linear but the same cannot be said of the payoff on an option contract. Indeed, above its exercise price, the payoff of a call option is linear but below it is horizontal therefore these properties mu ...

... The payoff of equities is linear and additive so that the payoff of a portfolio of equities is also linear but the same cannot be said of the payoff on an option contract. Indeed, above its exercise price, the payoff of a call option is linear but below it is horizontal therefore these properties mu ...

Risk Management Strategies

... Notice some features of this probability distribution. First, it is symmetric around the mid-point (20) of the range of all possible outcomes. That means that the probability of an outcome lower than the mid-point is 0.5 and the probability of an outcome occurring that is higher than the mid-point i ...

... Notice some features of this probability distribution. First, it is symmetric around the mid-point (20) of the range of all possible outcomes. That means that the probability of an outcome lower than the mid-point is 0.5 and the probability of an outcome occurring that is higher than the mid-point i ...

hedging volatility risk

... to deal with the risk that volatility itself may change. Volatility risk has played a major role in several financial disasters in the past 15 years. Long-Term-Capital-Management (LTCM) is one such example, “In early 1998, Long-Term began to short large amounts of equity volatility.” (Lowenstein, R. ...

... to deal with the risk that volatility itself may change. Volatility risk has played a major role in several financial disasters in the past 15 years. Long-Term-Capital-Management (LTCM) is one such example, “In early 1998, Long-Term began to short large amounts of equity volatility.” (Lowenstein, R. ...

Price Discrimination Law and Economic Efficiency

... economic efficiency only incidentally and accidentally, if at all. These difficulties do not arise from any supposed fact that price differences in real transactions must always rest upon foundations of economic efficiency. Often they do not. Instead, the difficulties arise from two quite different ...

... economic efficiency only incidentally and accidentally, if at all. These difficulties do not arise from any supposed fact that price differences in real transactions must always rest upon foundations of economic efficiency. Often they do not. Instead, the difficulties arise from two quite different ...

Clearing Trade Interface (CTI)

... block” is a valid configuration while “…except trades for badge 789-A” is not. Trade routing by firm names is not supported at this time either. If an order provider supplies a CMTA number, CMTA number will be used for routing decisions instead of the order provider’s default OCC clearing number. Fi ...

... block” is a valid configuration while “…except trades for badge 789-A” is not. Trade routing by firm names is not supported at this time either. If an order provider supplies a CMTA number, CMTA number will be used for routing decisions instead of the order provider’s default OCC clearing number. Fi ...

Slides

... Crisis (Enron, Worldcom) push new regulations (observability of derivatives) which was the first reason to push an index tranche market and base correlation ...

... Crisis (Enron, Worldcom) push new regulations (observability of derivatives) which was the first reason to push an index tranche market and base correlation ...

Long term spread option valuation and hedging

... of price cointegration together with the principal statistical tests for cointegration and the mean reversion of spreads. Section 3 proposes the two factor model for the underlying spot spread process and shows how to calibrate it. Section 4 presents option pricing and hedging formulae for options o ...

... of price cointegration together with the principal statistical tests for cointegration and the mean reversion of spreads. Section 3 proposes the two factor model for the underlying spot spread process and shows how to calibrate it. Section 4 presents option pricing and hedging formulae for options o ...

A Copula-Based Model of the Term Structure of CDO Tranches

... standard pricing tool in the market (the gaussian copula plays the role of the Black and Scholes formula in option pricing). ...

... standard pricing tool in the market (the gaussian copula plays the role of the Black and Scholes formula in option pricing). ...

Scalping Option Gammas - Dean Mouscher`s masteroptions.com

... tract rose. Consider what would happen if, instead of rising, the underlying contract went down. If the futures fell from 112 to 111 right after the initial purchase, the 112 calls would be worth $516 and the 112 puts would be worth $1,516, for a total position value of $101,600 and a profit of $7,8 ...

... tract rose. Consider what would happen if, instead of rising, the underlying contract went down. If the futures fell from 112 to 111 right after the initial purchase, the 112 calls would be worth $516 and the 112 puts would be worth $1,516, for a total position value of $101,600 and a profit of $7,8 ...

The 2008 Short Sale Ban`s Impact on Equity Option Markets

... Abstract. We examine how the confusion and regulatory uncertainty generated by the imposition of short sale restrictions in September 2008 impacted equity option markets. We uncover four primary findings. First, investors seeking short exposure in financial stocks did not migrate to the option marke ...

... Abstract. We examine how the confusion and regulatory uncertainty generated by the imposition of short sale restrictions in September 2008 impacted equity option markets. We uncover four primary findings. First, investors seeking short exposure in financial stocks did not migrate to the option marke ...

Hedging Barrier Options - Homepages of UvA/FNWI staff

... In contrast, when claims cannot be perfectly replicated by trading marketable assets, any hedging strategy leaves some residual risk and investors’ attitudes toward risk affect the pricing of the claims. For example, Hull and White (1987) introduce stochastic volatility in a model otherwise similar ...

... In contrast, when claims cannot be perfectly replicated by trading marketable assets, any hedging strategy leaves some residual risk and investors’ attitudes toward risk affect the pricing of the claims. For example, Hull and White (1987) introduce stochastic volatility in a model otherwise similar ...

NBER WORKING PAPER SERIES RESOLVING MACROECONOMIC UNCERTAINTY IN STOCK AND BOND MARKETS

... the sample period of the economic derivatives data. These options are American-style and Datastream thus computes their implied volatilities using a binomial model. We also obtain prices of options on the 5-year Treasury note futures directly from the CBOT, where they are traded, and compute implied ...

... the sample period of the economic derivatives data. These options are American-style and Datastream thus computes their implied volatilities using a binomial model. We also obtain prices of options on the 5-year Treasury note futures directly from the CBOT, where they are traded, and compute implied ...

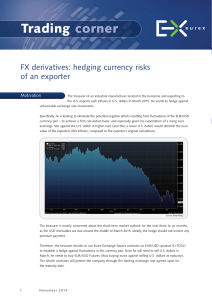

Trading Corner - Eurex Exchange

... the futures position is due to the fact that the hedge ratio is rounded from 78.31 to 78 contracts. ...

... the futures position is due to the fact that the hedge ratio is rounded from 78.31 to 78 contracts. ...

An Equilibrium Model of Catastrophe Insurance Futures and Spreads

... by the CBOT on October 18, 1994, that started trading the same year. These contracts— known as area yield options—provide a means for hedging against shortfall in the harvest of particular crops. An advantage of the crop yield contracts is that there is already an OTC derivatives market in this area ...

... by the CBOT on October 18, 1994, that started trading the same year. These contracts— known as area yield options—provide a means for hedging against shortfall in the harvest of particular crops. An advantage of the crop yield contracts is that there is already an OTC derivatives market in this area ...

The information content of interest rate futures options

... American-style2 call and put3 options written on the underlying ED futures contract. A 3-month ED futures call option gives the holder the right but not the obligation to buy a 3-month ED futures contract. Now, investors who expect U.S. short-term interest rates to decline would also be expecting th ...

... American-style2 call and put3 options written on the underlying ED futures contract. A 3-month ED futures call option gives the holder the right but not the obligation to buy a 3-month ED futures contract. Now, investors who expect U.S. short-term interest rates to decline would also be expecting th ...

The information content of interest rate futures options

... American-style2 call and put3 options written on the underlying ED futures contract. A 3-month ED futures call option gives the holder the right but not the obligation to buy a 3-month ED futures contract. Now, investors who expect U.S. short-term interest rates to decline would also be expecting th ...

... American-style2 call and put3 options written on the underlying ED futures contract. A 3-month ED futures call option gives the holder the right but not the obligation to buy a 3-month ED futures contract. Now, investors who expect U.S. short-term interest rates to decline would also be expecting th ...